Most people celebrate buying their first home as a financial milestone. For founders managing serious capital, it's just the opening move.

The Knight Frank Wealth Report paints an interesting picture. Around 81% of ultra-high-net-worth individuals own their primary residence. That part isn't surprising. What caught the attention: 30% actively invest in additional properties, and nearly half of family offices plan to increase their real estate allocations over the next 18 months.

Why does property hold such a grip on serious wealth?

Because real estate isn't just an asset class. It's a system. One that generates income, fights inflation, comes with substantial tax advantages, and can scale across borders when structured properly. The catch? Most resources either oversimplify ("just buy rental properties!") or assume institutional-level sophistication.

Let's explore the gap between those two extremes.

What's Inside

- Tax arbitrage is real: Depreciation, 1031 exchanges, and interest deductibility mean a 6% gross yield can deliver 8%+ after-tax returns

- UK landlords face headwinds: Section 24 caps mortgage relief at 20%, CGT allowance sits at £3,000, and the 5% stamp duty surcharge makes holding structure planning essential

- Geographic concentration kills portfolios: Wealthy investors hold property in 3+ countries — for currency, political, and market cycle diversification

- Singapore is closed to foreign residential buyers: 60% ABSD makes entry prohibitive. Dubai charges 4% transfer fee and 0% on everything else

- Leverage sweet spot: Target 50-65% LTV on stabilised properties. At 80% LTV, a 20% value decline wipes out all equity

- Access routes matter less than strategy: Direct ownership, REITs, syndications, or tokenised assets — pick based on control needs, liquidity requirements, and operational tolerance

- Family offices target 13.8% unleveraged returns: Achieved through income yield, rent growth, and modest leverage — not speculation

Why Investors Like Property

What makes real estate different from other investments comes down to three characteristics that compound over time.

Inflation Hedge

Real estate is tangible. You can touch it, walk through it, improve it. Its value is tied to actual land and buildings rather than to market sentiment alone.

When prices rise, rents typically follow. When construction costs increase, existing properties become more valuable. This isn't theoretical. According to CBRE research, commercial property fundamentals have remained stable through recent inflationary periods, with same-store net operating income growth for REITs projected at around 3% for 2025.

Inflation protection occurs on two fronts: capital appreciation (property values rise with replacement costs) and income (leases often include rent escalation clauses tied to inflation indices).

Predictable Income

Residential and commercial properties generate contractual income. Tenants sign leases. They pay monthly. The cash flow is more predictable than dividends from most public equities.

Some sectors proved remarkably resilient through recent volatility. Multifamily housing barely noticed the pandemic disruption. Logistics centres thrived on e-commerce acceleration. Healthcare real estate stayed solid through the chaos. The FTSE Nareit All Equity REIT Index delivered 14% total returns in 2024, though the picture was more mixed in 2025 — the same index returned just 2.3% for the full year, with healthcare REITs leading at 28.5% and industrial at 17.0%, according to Nareit data.

That isn't speculative income. It's contractual cash flow hitting accounts on a schedule. The year-to-year variation in REIT returns reinforces why real estate works best as a long-duration holding, not a trade.

Tax Advantages

Here's where real estate gets genuinely interesting for founders with liquidity.

Depreciation creates phantom losses. In the US, you can write off your building's value over time, cutting your tax bill while the property actually appreciates. The IRS lets you claim deductions on something that makes you money. It's one of the few remaining legal tax arbitrage opportunities for individual investors.

1031 exchanges defer gains indefinitely. Section 1031 of the Internal Revenue Code allows investors to sell one investment property and buy another of equal or greater value while deferring all capital gains taxes. According to the American Bar Association, this provision has existed since the Revenue Act of 1921. The tax deferral compounds over multiple exchanges. More importantly, if someone dies holding the replacement property, heirs receive a stepped-up basis. The deferred gains simply disappear.

Interest deductibility subsidises borrowing. Finance costs remain deductible against property income in most jurisdictions, effectively meaning the government subsidises part of borrowing costs.

The after-tax returns from real estate often look dramatically different from pre-tax headline numbers. A property yielding 6% gross might deliver 8%+ after accounting for depreciation shields and leverage effects.

UK-Specific Considerations: The tax landscape for UK landlords has shifted over the past few years. Since the Section 24 reforms, mortgage interest relief is capped at the basic rate (20%) regardless of income tax band. Capital Gains Tax on residential property sits at 18% for basic-rate taxpayers and 24% for higher-rate taxpayers, with the annual CGT allowance at just £3,000 for 2025/26. The stamp duty surcharge on additional properties stands at 5% following the October 2024 Budget. These changes make holding structure planning essential for UK-based investors. For more on how different jurisdictions handle tax, see our tax frameworks for global founders.

Commercial vs. Residential

The choice between commercial and residential property isn't binary. Most sophisticated portfolios include both, weighted according to specific objectives.

Commercial Real Estate

Around 19% of UHNW individuals plan to invest in commercial real estate in any given year, according to Knight Frank's Attitudes Survey.

The sectors generating most interest right now:

Logistics and warehousing have been the standout performers. E-commerce penetration hit a record 23.2% of total US retail sales in Q3 2024 and is projected to reach 25% by the end of 2025, according to CBRE. E-commerce utilises three times as much warehouse space as traditional retail. The structural tailwinds are real, though supply has caught up in some markets.

Healthcare real estate benefits from demographic certainty. Ageing populations need clinics, assisted living facilities, and medical offices. Healthcare REITs returned 28.5% in 2025 — the best-performing REIT sector by a wide margin.

Data centres represent the intersection of real estate and technology infrastructure. Equinix and Digital Realty have delivered over 2,800% total returns over the past two decades, according to Nareit data. The AI infrastructure buildout only accelerates demand.

Offices remain polarised. Trophy assets in prime locations with ESG credentials are performing. Generic suburban offices face structural headwinds from hybrid work. Vacancy rates appear to have peaked in late 2025, with the inflexion point becoming more visible as the vast majority of office occupants have now adjusted their footprints post-pandemic. But office REITs still posted a negative full-year return in 2025.

Commercial deals typically involve larger capital requirements, longer holding periods, and more complex due diligence. The potential returns often justify the complexity.

Residential Keeps Working in Supply-Constrained Markets

Higher interest rates haven't killed prime residential markets. London, Singapore, Dubai, Miami, and other global cities remain structurally undersupplied. Too many buyers chasing too few properties.

The Knight Frank Prime Global Cities Index (Q3 2025) tells a nuanced story. Tokyo led the global ranking with annual price growth of 55.9%, driven by limited resale supply and surging foreign investment. Seoul followed at 25.2%, with Dubai maintaining 8.5% annual growth, though seeing a sharp quarterly decline. Average annual growth across the 46 tracked cities slowed to 2.5%, down from a long-term trend of 5.2%. The picture varies enormously by city.

Smart money in residential focuses on:

Build-to-rent developments, where institutional capital is displacing traditional landlords. The sector has matured rapidly with strong fundamentals.

Multifamily housing in growing cities with supply constraints and population growth. Residential real estate remains the most popular sector among family offices, with 81% of family offices investing in it, according to industry surveys.

Strategic lifestyle purchases that serve dual purposes: personal enjoyment plus capital preservation in stable jurisdictions.

The appeal of residential is universality. Everyone understands housing. Everyone needs somewhere to live. The asset class is less complex to underwrite than commercial property.

Everything here is free. Subscribing just tells me the content is useful — and helps me decide what to write next.

Geographic Diversification: Beyond Your Home Market

Concentration risk destroys portfolios. It's the same lesson whether we're talking about public equities or property holdings. This applies directly to how founders should think about investment philosophy in uncertain markets.

According to Knight Frank research, wealthy investors typically hold property in three or more countries. This isn't just about chasing returns. It's about managing currency exposure, political risk, and market cycle correlation.

Different Jurisdictions, Different Rules

United Kingdom offers strong legal protections and property rights. Transaction costs are meaningful, though. Stamp duty for additional properties now includes a 5% surcharge. Non-residents face additional complexities. Rental yields in certain cities remain attractive, and the legal system provides certainty that many other jurisdictions can't match.

Dubai and Singapore make it easier for foreign investors in different ways. Minimal property taxes, transparent processes, expat-friendly ownership rules. Dubai maintained strong prime residential growth through 2024 and into 2025, though valuations have caught up with fundamentals in some segments. For more on comparing jurisdictions, see our family office location guide.

Switzerland offers stability, but good luck finding anything available. Foreign ownership restrictions (the Lex Koller law) make entry difficult. What you get in exchange: political neutrality, strong currency, and wealth preservation infrastructure.

Portugal attracted significant capital through its golden visa programme, though recent changes have reduced property investment options. The Non-Habitual Resident regime was eliminated for new applicants from 2024. The Golden Visa no longer accepts residential property investment in Lisbon or Porto.

Know the rules before committing capital. Legal systems, ownership restrictions, taxation of foreign owners, and repatriation of funds vary dramatically.

Currency Risk Is Real (And Often Ignored)

That London flat might appreciate 10%. Excellent news, unless sterling drops 15% against your base currency. Suddenly, you've lost money in real terms.

Sophisticated investors hedge currency exposure through forward contracts, multi-currency mortgages, or simply spreading holdings across currency zones. The goal isn't eliminating currency exposure entirely. It's about managing it consciously rather than taking concentrated bets by accident.

Structure Matters From Day One

Cross-border portfolios require planning before the first purchase:

Holding company structures in appropriate jurisdictions (such as Luxembourg, BVI, or Jersey) can offer tax efficiency and estate planning benefits. Get advice before buying rather than attempting to restructure later.

International trusts serve estate planning purposes, removing assets from your personal estate while maintaining some control. The structures differ by jurisdiction. For a deeper look at how structures work, the family office playbook covers governance and wealth architecture in detail.

Tax treaty optimisation becomes material at scale. Double taxation treaties between countries determine how income and gains are taxed. Structure affects outcomes significantly.

The cost of good international tax advice typically pays for itself many times over.

How to Access Real Estate: Three Main Routes

There's no single correct way to invest in property. Each approach involves trade-offs between control, liquidity, capital requirements, and operational burden.

Route 1: Direct Ownership

Buying and holding physical property offers the greatest control and typically the highest gross returns. You decide when to sell, how much leverage to use, when to renovate, and which tenants to accept.

The trade-offs: time commitment, operational complexity, concentration risk, and illiquidity. Managing five properties across four countries requires either significant personal bandwidth or reliable third-party management.

Direct ownership works best when you have a genuine interest in the asset class, the ability to add value through local knowledge or relationships, sufficient scale to justify the operational overhead, and tolerance for illiquidity.

Route 2: REITs (Public and Private)

Real Estate Investment Trusts own and operate income-producing real estate across multiple property sectors. In the US alone, there are approximately 225 publicly traded REITs covering sectors from residential to healthcare to data centres.

The appeal is straightforward: liquidity (publicly traded REITs can be sold immediately), diversification (one holding gives exposure to hundreds of properties), professional management, and no operational burden. REITs also tend to pay attractive dividends. As of year-end 2025, all equity REITs offered dividend yields of 4.07% according to Nareit, with mortgage REITs offering 12.2%.

The drawbacks are equally clear: less control, fee drag from management expenses, and correlation with public equity markets during stress periods. When stocks sell off, publicly traded REITs often follow regardless of underlying property fundamentals.

REITs have historically delivered competitive total returns. The 25-year average annual return has been approximately 10-12%, with about half of total returns coming from dividends, according to Nareit research.

Private REITs offer another option: similar diversification benefits without daily pricing volatility. The trade-off is reduced liquidity and typically higher minimum investments. For more on evaluating private market investments, see our private equity guide for HNW investors.

Route 3: Private Funds and Syndications

Want to buy a €50 million shopping centre? You probably can't do it alone. Pool capital with nine other investors, and suddenly it's feasible.

Syndications and club deals provide access to institutional-quality assets without requiring institutional capital. Family offices favour these structures. PwC research shows that 69% of family office investments in the first half of 2025 were "club deals" (investing alongside others) rather than sole investments.

Private funds work well for mid-market commercial assets, development projects where expertise matters, niche sectors like data centres, cold storage, or student housing, and situations requiring speed or relationship access.

The considerations: illiquidity (typically 7-10 year holds), performance dispersion across managers, fee structures, and limited control over asset-level decisions.

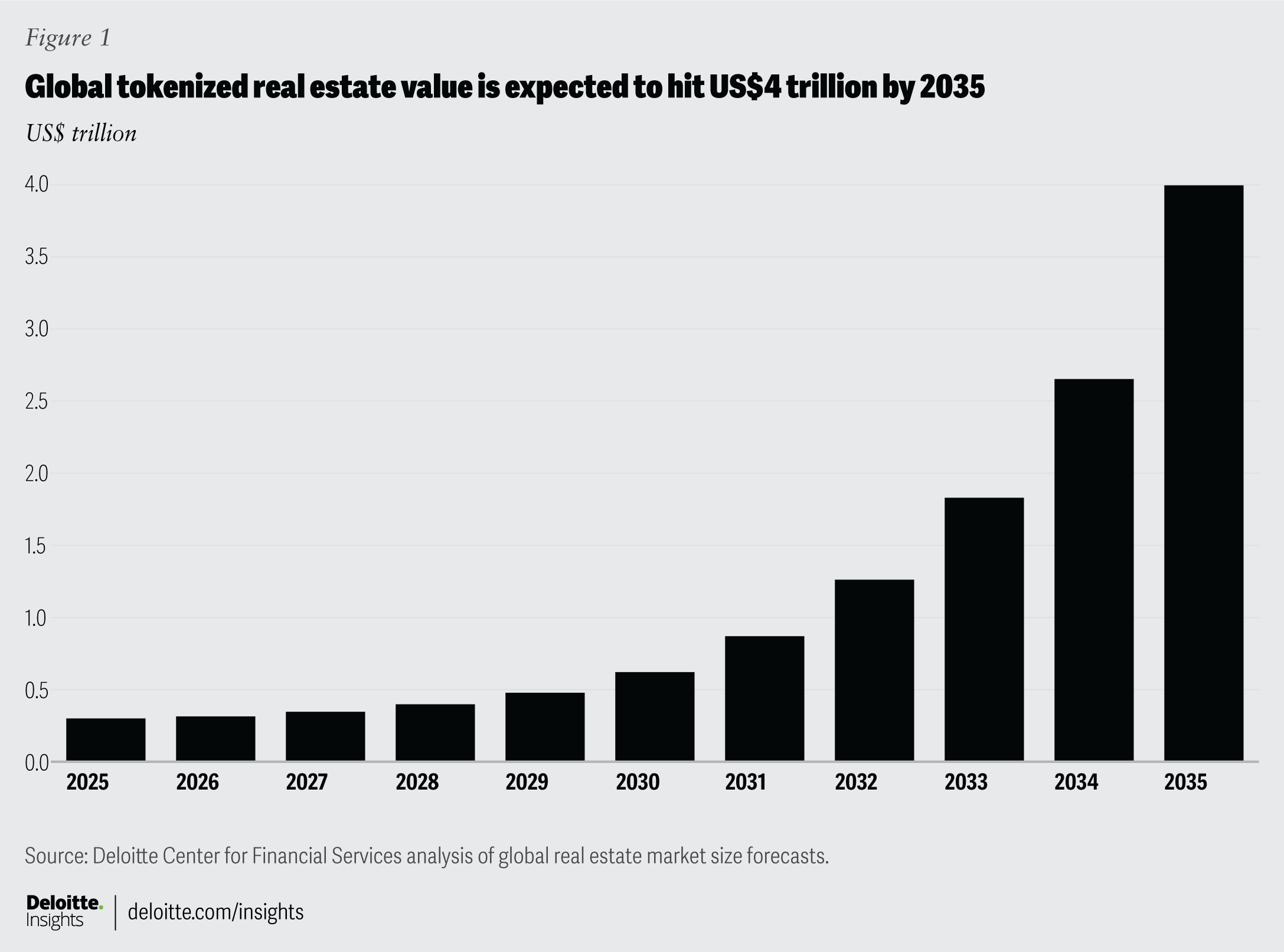

Emerging Option: Tokenised Real Estate

Blockchain technology enables fractional ownership of property through digital tokens. A €10 million Paris commercial building can be divided into tokens representing small ownership stakes, tradeable on secondary markets with settlement in days rather than months.

The space has matured considerably. The global tokenised real estate market reached approximately $20 billion by 2025, accounting for roughly 30% of all tokenised asset issuance. Deloitte found that 12% of real estate firms globally had implemented tokenisation solutions by mid-2024, with another 46% piloting programmes. The passage of the US GENIUS Act in July 2025 brought regulatory clarity to the stablecoin rails on which tokenised assets depend, and the EU's MiCA regulation is now fully live.

What tokenisation solves: Traditional real estate's liquidity problem. Properties typically take months to sell. Tokenised stakes can trade in days, though secondary-market depth remains limited.

What it doesn't solve (yet): Secondary markets for real estate tokens are still thin. Regulatory frameworks exist now in the US, EU, UAE, and Singapore, but harmonisation across jurisdictions remains incomplete. The infrastructure is maturing quickly, but institutional adoption is still in the early stages.

Industry projections suggest the real estate tokenisation market could grow from roughly $3.5 billion in dedicated platforms in 2024 to over $4 trillion by 2035, according to Deloitte forecasts. Whether those numbers prove accurate depends on continued regulatory development and secondary market liquidity.

For now, tokenised real estate represents an interesting addition to allocation options rather than a replacement for traditional structures.

Leverage: The Double-Edged Sword

Debt amplifies returns. It also amplifies losses. Getting leverage right matters more than most acquisition decisions.

The Numbers That Matter

Most sophisticated investors target loan-to-value ratios of 50-65% for stabilised properties. Enough leverage to enhance returns meaningfully. Not so much that a modest valuation decline wipes out equity.

At 50% LTV, a 20% property value decline leaves you with 60% of your equity intact. At 80% LTV, the same decline eliminates all equity and likely triggers covenant breaches.

Interest rates matter more at higher leverage levels. The difference between 5% and 7% financing costs barely registers on an unleveraged property. On a property with 75% leverage, that 200 basis point difference might eliminate half your cash-on-cash return.

Match Financing to Strategy

Different property types and strategies warrant different financing approaches:

Stabilised income properties support longer-term fixed-rate debt. You want certainty matching predictable income.

Value-add or development projects typically use floating-rate construction loans, with refinancing upon stabilisation.

Cross-border holdings may benefit from local currency financing that provides natural currency hedges. Borrowing euros to buy Paris property reduces currency mismatch versus financing in dollars.

Interest-only periods provide cash flow flexibility during the initial ownership period but result in no principal paydown. Understand what you're accepting.

Making It Work at Scale

Managing five properties is manageable. Fifteen properties across four countries require infrastructure.

Operational Stack

Professional property portfolios need:

Management partnerships with firms that have a genuine presence in your target markets. Local knowledge matters. The best London property manager likely isn't the right choice for Miami holdings.

Consolidated reporting that provides portfolio-level visibility rather than property-by-property updates. Platforms exist specifically for this purpose.

Tax coordination across jurisdictions to ensure structures remain optimal as rules change. This requires advisors who communicate across borders.

Governance frameworks that define decision rights, approval thresholds, and reporting requirements. Who approves capital expenditure above £50,000? Who decides when to sell? Define these before questions arise. The governance chapter in our family office playbook covers this in detail.

What Family Offices Actually Do

According to Knight Frank's survey of 150 family offices, real estate fulfils different objectives in their broader portfolios: growth and capital appreciation (42%), wealth preservation (23%), and income generation (19%).

The average target unleveraged return is 13.8%. Most achieve this through a combination of income yield, rent growth, and modest leverage — not speculation.

Family offices typically blend approaches rather than picking one: direct investments in markets they know well, private fund exposure for diversification into unfamiliar sectors or geographies, and REIT allocations for liquidity.

Where to Focus in 2026

Based on current market conditions, several themes deserve attention.

Logistics and industrial fundamentals remain strong despite some supply catch-up. E-commerce penetration continues to grow. Nearshoring trends benefit warehousing near manufacturing hubs. Class A modern facilities with high ceilings and automation capability command premium rents and occupancy. Industrial REITs returned 17% in 2025.

Residential in supply-constrained markets continues performing. Housing shortages across major economies drive both rental and price growth. Build-to-rent institutionalisation creates exit options that didn't exist a decade ago. Knight Frank's Q3 2025 data shows average prime city price growth cooling to 2.5% annually, which may present opportunities as rate cuts take hold in 2026.

Opportunistic office for those with conviction. Prices remain well below peaks, and vacancy rates appear to have turned a corner. If you believe hybrid work has stabilised at current levels rather than continuing toward fully remote, the entry point could be attractive. High conviction required, though — office REITs were negative again in 2025.

Healthcare real estate benefits from demographic tailwinds that are visible decades ahead. Ageing populations need care facilities. New supply is constrained by regulation and complexity. Healthcare was the top-performing REIT sector in 2025 at 28.5%.

Tokenised real estate as a small allocation for those wanting exposure to the technology evolution. Treat it as venture-style allocation rather than core real estate. The regulatory picture has improved significantly with the US GENIUS Act and EU MiCA now live.

Illustrative Portfolio: £15M Property Allocation

This section walks through how an investor with £15 million in liquid assets might structure a property portfolio. This is illustrative — not prescriptive. Every situation differs.

Starting Point

A founder sold their fintech company eighteen months ago. After taxes, £15 million in cash and liquid securities. Owns a London home outright (worth approximately £3 million) but has no investment property experience. Objectives: generate £300,000+ annual income, preserve capital across generations, and build something that runs without consuming time.

Allocation Framework

Working with advisors, they developed this target allocation:

Direct UK Property (£4 million, 27%). Two prime London apartments in zones 1-2, each valued at around £2 million. Target gross yield: 3.5-4%. These serve as core holdings in a market they understand deeply. Management outsourced to a local firm charging 12% of gross rent. Expected net yield after costs: approximately 2.8%, or £112,000 annually. Lower yields are acceptable for core holdings with strong capital-preservation characteristics.

European Commercial via Fund (£3 million, 20%). Commitment to a diversified European logistics fund managed by an established operator. Target net IRR: 12-14% over a 7-year hold. For someone without expertise in continental warehousing, engaging a specialist manager makes sense. Capital calls spread over 18 months. The fund focuses on last-mile logistics facilities in Germany, Netherlands, and France. Typical fee structure: 1.5% management fee plus 20% carried interest above an 8% hurdle.

US Multifamily Syndication (£2.5 million, 17%). Two syndication investments: one in Austin (£1.5 million) focusing on value-add multifamily, another in Phoenix (£1 million) targeting new development. Both structured as Delaware LLCs with the investor as limited partner. Target returns: 15-18% IRR over 5-year holds. Higher risk than the London apartments, but significant upside if execution goes well.

Public REITs (£2 million, 13%). Diversified REIT portfolio split across sectors: 40% industrial/logistics, 25% residential, 20% healthcare, 15% data centres. This provides immediate liquidity, sector diversification beyond the direct holdings, and income (approximately 4% yield, or £80,000 annually). Tax-advantaged wrappers (ISA, pension) where possible to shelter REIT income from UK tax.

Dubai Apartment (£1.5 million, 10%). One luxury apartment in a prime Marina location. Purchased for lifestyle use with rental income when not occupied. No annual property tax, no capital gains tax on eventual sale. Expected rental yield when let: 5-6%. Also provides geographic diversification outside Europe and sterling.

Tokenised Real Estate (£500,000, 3%). Small allocation to tokenised commercial property through a regulated platform. Venture-style exposure to the technology evolution rather than core real estate.

Cash Reserve (£1.5 million, 10%). Held for opportunistic acquisitions, capital calls on fund commitments, and general liquidity.

The Numbers

| Holding | Value | Expected Yield | Annual Income |

|---|---|---|---|

| London Apartments | £4.0M | 2.8% net | £112,000 |

| European Logistics Fund | £3.0M | N/A (IRR target) | Reinvested |

| US Multifamily | £2.5M | N/A (IRR target) | Reinvested |

| REIT Portfolio | £2.0M | ~4.0% | £80,000 |

| Dubai Apartment | £1.5M | 4.0% net (when let) | £60,000 |

| Tokenised RE | £0.5M | Variable | Variable |

| Cash | £1.5M | ~4.5% | £67,500 |

| Total | £15.0M | £320,000+ |

The income target of £300,000 is met from day one, with significant additional returns expected from the fund and syndication investments as they mature.

Structure Decisions

UK properties held personally (simplest approach given current scale). The Dubai apartment in a BVI company for estate planning purposes. US investments through Delaware LLCs. Fund and REIT investments held partly in tax-advantaged accounts.

Total annual advisory costs: approximately £25,000 for tax structuring, £15,000 for property management, and £8,000 for consolidated reporting. About £48,000 total, or 0.32% of assets. Reasonable for the complexity involved.

How This Might Play Out

The reality of any portfolio like this will diverge from projections. Some holdings will outperform expectations — perhaps the logistics fund benefits from a surge in e-commerce infrastructure spend, or the Dubai apartment catches a cycle perfectly. Others will underperform — construction delays in a US syndication, or a REIT sector rotation that drags returns down for a year.

The point isn't that every line item hits its target. The point is that the structure — diversified across geographies, sectors, access routes, and liquidity profiles — absorbs shocks without requiring the investor to spend more than a few hours monthly on oversight. The machine runs with minimal intervention.

This example is purely illustrative and does not constitute investment advice. Actual returns will vary based on market conditions, timing, and individual circumstances. Always consult qualified professionals before making investment decisions.

Due Diligence Checklist

Before committing capital to any real estate investment, work through these questions systematically. Skip nothing.

For Direct Property Purchases

Market Fundamentals

- What's the vacancy rate in this submarket? Trend over five years?

- Net migration patterns: is the population growing or shrinking?

- Major employers in the area: concentration risk?

- New supply pipeline: what's under construction within 3km?

- Historical rent growth: compound annual rate over 10 years?

Property Specifics

- When was the building constructed? Major systems ages (roof, HVAC, elevators)?

- Deferred maintenance estimate from an independent inspector?

- Current tenant roster: lease terms, renewal history, creditworthiness?

- Tenant concentration: does any single tenant exceed 25% of income?

- Historical operating expenses: trend over three years?

- Environmental issues: Phase I assessment completed?

Financial Analysis

- Cap rate relative to comparable recent sales?

- Rent per square foot versus market average?

- Operating expense ratio: reasonable for property type?

- Capital expenditure forecast for next five years?

- Stress test: what happens if vacancy doubles?

Legal and Structural

- Title clear? Encumbrances understood?

- Zoning permits current use? Risks of changes?

- Any pending litigation involving the property?

- Holding structure appropriate for your tax situation?

- Exit options: who would buy this property?

For Fund or Syndication Investments

Manager Assessment

- Track record: actual realised returns on prior funds (not just IRR projections)?

- Team stability: key person risk?

- Assets under management: are they capacity constrained?

- Alignment: how much of their own capital is invested?

- References from existing LPs?

Strategy Fit

- Does the strategy match current market conditions?

- Vintage year risk: are they deploying capital at market peaks?

- Geographic focus: markets you understand and believe in?

- Leverage policy: maximum LTV? Recourse vs. non-recourse?

Terms and Fees

- Management fee: reasonable for the strategy?

- Carried interest: threshold rate? Catch-up provisions?

- Preferred return structure?

- Fee offsets for transaction or property management fees?

- Key person provisions: what happens if principals leave?

Legal Protections

- LPAC (Limited Partner Advisory Committee) rights?

- Excuse and exclusion provisions?

- Reporting requirements: frequency and detail?

- Audit requirements?

- Transfer restrictions: can you sell your interest?

For REIT Investments

Company Quality

- Balance sheet strength: debt-to-EBITDA ratio?

- Interest coverage ratio?

- Weighted average debt maturity?

- Dividend coverage: FFO payout ratio?

- Track record of dividend growth?

Portfolio Quality

- Asset quality: average age, location grades?

- Tenant quality: average credit rating?

- Lease duration: weighted average lease term?

- Occupancy rates versus peers?

- Same-store NOI growth history?

Valuation

- Price-to-FFO relative to historical average?

- Premium or discount to NAV?

- Dividend yield relative to sector average?

- Implied cap rate versus private market transactions?

Property Tax Comparison: Six Key Jurisdictions

Tax treatment varies dramatically across markets. This table summarises the key taxes affecting property investors in six popular jurisdictions. Rates current as of early 2026.

United Kingdom

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (Stamp Duty) | 0-12% + 5% surcharge | Surcharge applies to additional properties over £40,000 |

| Annual Property Tax | Council Tax varies | Based on property band, location; £1,500-5,000+ typical |

| Rental Income Tax | 20/40/45% | Personal rates; mortgage interest capped at 20% relief |

| Capital Gains Tax | 18% or 24% | £3,000 annual allowance (2025/26) |

| Inheritance Tax | 40% | Above £325,000 threshold (or £500,000 with residence nil-rate) |

Key Consideration: Section 24 mortgage interest restrictions make corporate structures worth evaluating for portfolio landlords. The CGT allowance at £3,000 (down from £12,300 a few years ago) significantly increases tax on sales.

United States

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (Transfer Tax) | 0.1-2.5% | Varies dramatically by state |

| Annual Property Tax | 0.5-2.5% | Of assessed value; varies by state/county |

| Rental Income Tax | 10-37% | Federal rates; plus state tax; depreciation offsets |

| Capital Gains Tax | 0-20% + 3.8% NIIT | Long-term rate; depreciation recapture at 25% |

| Estate Tax | 40% | Above $15 million federal exemption (2026) |

Key Consideration: Depreciation (27.5 years residential, 39 years commercial) significantly reduces the current tax burden. 1031 exchanges allow indefinite deferral of capital gains. The federal estate tax exemption rose to $15 million per individual in 2026 under the One Big Beautiful Bill Act, permanently indexed for inflation. State taxes vary enormously.

Dubai (UAE)

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (Transfer Fee) | 4% | Split equally buyer/seller in practice |

| Annual Property Tax | 0% | No annual property tax |

| Rental Income Tax | 0% | No personal income tax |

| Capital Gains Tax | 0% | No capital gains tax |

| Inheritance Tax | 0% | No inheritance tax (Sharia law may apply) |

Key Consideration: Extremely tax-efficient for holding period returns. Foreigners can only purchase in designated freehold zones. Registration fees and service charges are the main ongoing costs. 5% municipality tax on rental value paid by tenants.

Singapore

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (BSD + ABSD) | 4-6% BSD + 60% ABSD | ABSD for foreigners is 60%; citizens 0% on first property |

| Annual Property Tax | 0-36% | Of annual value; owner-occupied rates lower |

| Rental Income Tax | 0-24% | Progressive rates; deductions available |

| Capital Gains Tax | 0% | No capital gains tax |

| Estate Tax | 0% | Abolished in 2008 |

Key Consideration: The 60% ABSD makes Singapore residential essentially prohibitive for foreign investors. Commercial and industrial properties are exempt from ABSD. No capital gains tax makes long-term holds attractive despite high entry costs.

Portugal

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (IMT + Stamp) | 0-8% IMT + 0.8% stamp | IMT varies by property value and type |

| Annual Property Tax (IMI) | 0.3-0.45% | Of tax value (VPT); municipalities set rate |

| Rental Income Tax | 25-28% flat or progressive | Can elect flat 25-28% or add to income |

| Capital Gains Tax | 50% taxed at marginal rate | Residents: 50% of gain added to income (14.5-48%) |

| Inheritance Tax | 0% (direct family) | 10% stamp duty for others |

Key Consideration: NHR regime eliminated for new applicants from 2024. Golden Visa no longer accepts residential property investment in Lisbon/Porto. IMI rates are low but AIMI (additional) wealth tax applies to holdings over €600,000.

Switzerland

| Tax Type | Rate | Notes |

|---|---|---|

| Purchase (Transfer Tax) | 0-3.3% | Varies by canton |

| Annual Property Tax | 0.05-0.3% | Of assessed value; very low |

| Rental Income Tax | 0-40%+ | Progressive cantonal + federal rates |

| Capital Gains Tax | 0% (federal) | Cantons may tax; often exempt if held >2 years |

| Wealth Tax | 0.3-1% | Annual tax on net worth; varies by canton |

Key Consideration: Foreign ownership severely restricted under Lex Koller law. Those who qualify benefit from low property taxes but face wealth tax on net worth. Lump-sum taxation available for non-working foreign residents in some cantons.

Quick Comparison Summary

| Jurisdiction | Entry Cost | Annual Cost | Exit Cost | Foreign-Friendly |

|---|---|---|---|---|

| UK | High (17%+) | Medium | Medium (24%) | Yes |

| US | Low-Medium | Medium-High | Low-Medium | Yes |

| Dubai | Low (4%) | Very Low | None | Yes |

| Singapore | Very High (64%+) | Medium | None | Residential: No |

| Portugal | Medium (9%) | Low | Medium | Yes |

| Switzerland | Low (3%) | Very Low | Very Low | Very Limited |

Entry costs include stamp duty/transfer taxes on a £1M+ property. Annual costs reflect property taxes. Exit costs reflect capital gains tax.

Exit Strategy Framework

Every property investment needs an exit plan. Not because you expect to sell soon, but because clarity about eventual disposition shapes decisions throughout the holding period.

Four Exit Paths

Path 1: Sale to Third Party. The most common exit. Sell on the open market to an unrelated buyer. Works best when market conditions favour sellers, the property has appreciated significantly, or you need liquidity for other opportunities. Consider transaction costs (agent fees of 1-3%, legal fees, potential CGT), realistic timing (3-12 months depending on asset type), and 1031 exchange potential in the US. Maintain property condition, keep tenant relationships strong, and build relationships with potential buyers before you need them.

Path 2: Refinance and Hold. Extract equity through refinancing rather than selling. The property stays, but capital comes out. Tax-efficient since no CGT is triggered on refinancing. Works best when strong cash flow supports higher debt service and the property has appreciated significantly. Debt service coverage must remain healthy, and loan-to-value limits constrain how much can be extracted. Build banking relationships before you need to refinance.

Path 3: Transfer to Next Generation. Pass property to children or other heirs, either during lifetime or at death. Inheritance tax implications vary dramatically (UK: 40% above thresholds; US: federal exemption now $15 million per individual under the One Big Beautiful Bill Act, permanently indexed for inflation). Structure holdings appropriately from purchase through trusts or family investment companies. Discuss with heirs before committing them to illiquid assets.

Path 4: Contribution to Charitable Vehicle. Donate property to charity or contribute to a charitable remainder trust. Works best when philanthropic goals align with tax planning, especially with highly appreciated property with a low basis. Consider charitable deduction limitations and appraisal requirements.

Exit Timing Indicators

Sell signals include cap rates compressing to historically low levels, rent growth decelerating or turning negative, new supply overwhelming demand in your submarket, property reaching end of economic life (major capex looming), and better opportunities available elsewhere.

Hold signals include strong and growing cash flow, healthy market fundamentals, tax consequences of sale outweighing benefits, no better alternatives for the capital, and refinancing having already achieved liquidity objectives.

Glossary of Key Terms

For definitions of real estate terminology used in this post — cap rate, NOI, cash-on-cash return, IRR, LTV, DSCR, FFO, and more — see our Glossary.

Every property serves a purpose: cash flow, inflation protection, lifestyle, wealth transfer, or some combination. The best portfolios combine multiple access routes, balance geographic and sector exposure, maintain appropriate leverage, and match liquidity profiles to actual needs.

Whether the route is direct ownership, REITs, private funds, or tokenised assets matters less than having a coherent strategy. Buying opportunistically without a framework leads to portfolios that look like accidents.

Real estate rewards patience more than almost any other asset class. The founders who do this well aren't necessarily the ones with the best deal flow or the deepest market knowledge. They're the ones who built the infrastructure — governance, reporting, advisory relationships — before the first cheque was written.

Capital Founders OS is an educational platform for founders with $5M–$100M in assets. Frameworks for thinking about wealth — so you can make better decisions.

Explore more: Playbooks · Capital Signals · Wealth Architecture · Investment Strategy · Business Building · Life Design

Found this useful? Forward it to a founder who's thinking about this stuff. Got a question or disagree with something? Get in touch.

New here? Subscribe for one email a week.