This is Capital Signal Weekly — timely briefings on what's reshaping Capital Founders' strategy on wealth architecture, investment strategy, business building, and life design.

THIS WEEK IN 30 SECONDS

📈 The 2026 IPO pipeline is deep but cautious. 2025 delivered $44B in proceeds. Deloitte expects $55–65B in 2026. Only nine IPOs have priced so far this year — down 47% from 2025.

💰 Fintech funding rebounded 21% to $116B — on an eight-year low in deal volume. Capital is concentrating into fewer, larger companies. The implications run through every liquidity pathway.

🔄 Tender offers are replacing traditional exits. Decagon ($4.5B), ElevenLabs ($6.6B), Clay, Linear — AI startups are running employee secondaries instead of waiting for IPOs. The mechanics matter for both sides of the table.

🏋️ Longevity is becoming an asset class. Equinox's $40K/year programme has a 1,000+ waitlist. The global wellness market: $6.8T today, projected $10T by 2030.

The same dynamic is showing up everywhere at once — in IPO performance, in venture deal flow, in how companies choose to provide liquidity, and in where wealthy founders spend after exit.

Capital isn't disappearing. It's concentrating. Fewer companies are absorbing more of it. The ones that don't make the cut find every path to liquidity narrower than it was two years ago. And the companies that do make the cut are increasingly choosing to stay private, using tender offers and structured secondaries instead of IPOs to give their people cash.

Four stories this week. One signal running underneath all of them.

The IPO Window Is Open. The Money Still Isn't Moving.

After three years of near-silence, the IPO market reopened in 2025. Not with a bang, but with discipline.

Deloitte's 2026 IPO Market Outlook calls it an above-average year: approximately $44 billion in IPO proceeds, with technology leading. Investor appetite is centred on enterprise-focused businesses with durable revenue and credible profitability. The anything-goes era of 2021 did not return. Foley & Lardner's February 2026 analysis adds that policy-aligned sectors — AI, defence tech, crypto infrastructure, fintech — dominated the 2025 class.

Some debuts worked. Figma's first-day spike became the year's headline. Circle's listing triggered a wave of crypto IPOs, including Gemini, Figure Technology, and Bullish. Klarna and CoreWeave completed notable listings, too.

Others didn't. Performance dispersion was sharp enough that the 2025 class tells two completely different stories depending on which companies you look at.

The 2026 pipeline is deep — but it's worth reading the list for what it tells you about the market, not just the names.

Three potential category-defining IPOs could individually reshape 2026:

- SpaceX — expected to pursue one of the largest IPOs ever, with valuation estimates around $1.5 trillion. Internal communications suggest the listing would fund Starship's launch rate, space-based data centres, and a lunar base

- OpenAI — reportedly preparing a late-2026 or 2027 listing. CFO Sarah Friar has pointed to 2027 as more realistic. Valuation discussions range from $830B to $1T

- Anthropic — valuation target reportedly $350–500B, though no formal timeline is set, and the company has said it has "made no decisions about when or even whether to go public"

If any of these lists, Deloitte's $55–65 billion 2026 projection gets blown past. If none do, the year looks more modest.

A second tier of AI infrastructure and crypto companies tests whether the market supports scale below megadeal level: Databricks (reportedly IPO-ready, ~$134B valuation, $4.8B run-rate revenue up 55% YoY), Cerebras (targeting Q2 2026 at $23B after CFIUS clearance), Kraken (wrapping a $500M pre-IPO round at ~$15B), and Discord (confidential filing in January).

And then there are the counter-signals. Motive, the fleet management company, paused its IPO marketing efforts despite being well into preparation. Not everything that's "IPO-ready" is actually going. The government shutdown in October 2025 pushed several ready candidates into 2026, creating a pipeline backlog that may take quarters to clear — or may never fully materialise if market conditions shift.

Here's the tension nobody's talking about enough. The early 2026 data doesn't match the pipeline optimism. U.S. News reported that only nine IPOs have priced in the US so far this year — down 47% from the same period in 2025. Proceeds total $2.6 billion, a 31% decline. The Renaissance IPO ETF is down 2.9% year-to-date while the S&P 500 is up 1.9%.

Deep pipeline. Cautious execution. That gap is the story.

Forge Global's pipeline tracker flags a structural shift beneath the headline numbers: many 2025 IPOs served primarily as liquidity events for existing shareholders rather than as growth capital for the company. The percentage of shareholder liquidity increased in many offerings, allowing early investors and employees to sell more quickly rather than waiting for the typical 180-day lockup. When IPOs serve as exit mechanisms for existing shareholders rather than capital raises, it suggests that the pressure to return cash to LPs, employees, and early investors is driving IPO timing as much as company readiness.

Which connects directly to the next story.

For founders building toward a public listing: the 2025 lesson is clear. Valuation discipline is non-negotiable. The companies that succeeded had durable revenue, clean unit economics, and realistic pricing. The ones that struggled tried to command 2021 multiples in a market that isn't buying them.

For post-exit founders allocating capital: the 2026 IPO class will create entry points worth watching, particularly in AI infrastructure. But post-IPO performance dispersion means the first-day pop is not the return. Databricks, with its $4.8B run rate and 55% growth, is a different proposition than a crypto exchange listing on momentum alone. Treat them accordingly.

A successful Databricks or Cerebras IPO doesn't just create liquidity for their shareholders. It sets pricing benchmarks that cascade through the secondary market, affecting how your own private holdings — LP stakes, angel positions, employee equity — get valued.

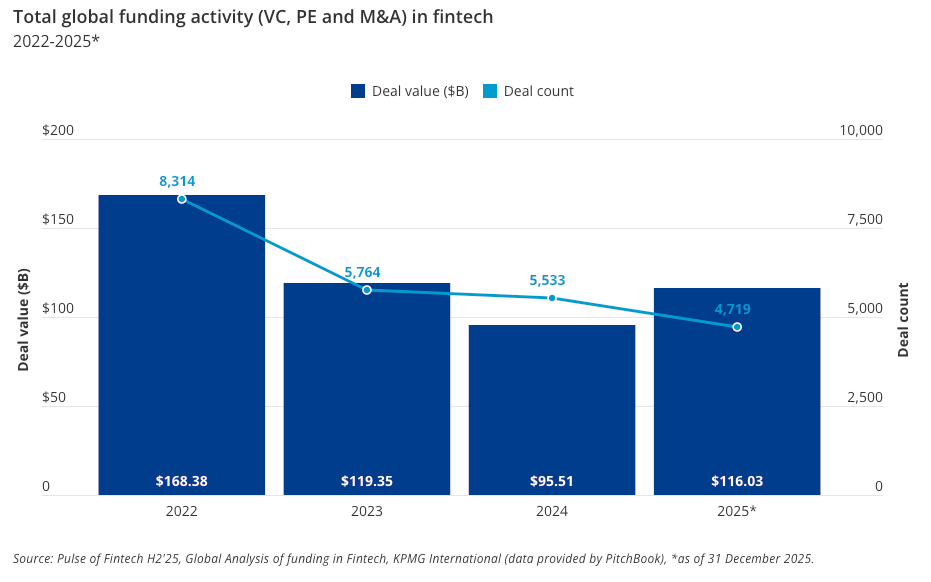

KPMG: 21% More Money. 15% Fewer Deals. What the Fintech Numbers Actually Mean.

KPMG's Pulse of Fintech H2 2025 confirmed what the venture market has been whispering for a year: capital is concentrating into fewer, larger bets. And the places where it's not going are as revealing as the places where it is.

Start with the divergence that matters most.

Global fintech investment rose 21% to $116 billion. Deal count fell 15% to 4,719 — the lowest since 2017. More money is flowing into fewer companies. Each surviving startup absorbed a larger share of available capital. The bar to get funded at all is substantially higher than it was two years ago.

That pattern is consistent across geographies — the Americas led with $66.5 billion (up from $55.4B), EMEA hit $29.2 billion (up from $26.5B). But Asia-Pacific declined from $11.7 billion to $9.3 billion, a signal that the concentration dynamic isn't just about selectivity. It's also geographic. Capital is flowing toward the US and Europe and away from markets where regulatory or macro headwinds create uncertainty.

Now look at where the money went — and where it didn't.

Digital assets nearly doubled, from $11.2 billion to $19.1 billion — the third-highest year on record. The GENIUS Act accelerated stablecoin and crypto infrastructure investment in H2 2025. AI-focused fintech grew from $12.1 billion to $16.8 billion. B2B products and services hit $13.5 billion, their strongest showing since 2019.

Payments — historically fintech's biggest draw — fell to $19.2 billion, a nine-year low, amid a decline in deal volume. Even the sector that built fintech is contracting.

And then there's wealthtech.

Total global wealthtech investment collapsed from a record $4.9 billion in 2024 to $1.4 billion in 2025. Down 71%. KPMG attributes the drop to a lack of emergent use cases and a rapid shift in investor attention toward AI. The largest wealthtech deal in H2 2025 was Wealthsimple's $538 million round at a $7.2 billion valuation — a single outlier in an otherwise barren landscape.

That number should concern anyone in the $5M–$100M range who relies on technology-driven wealth management. The tools managing your portfolio are attracting less investment precisely when portfolios are getting more complex — more alternative allocations, more private credit (and more questions about that private credit), more cross-border structures. The gap between what founders need from wealth management technology and what the industry is actually building may be widening in real time.

The data in brief:

- Fintech investment: $116B (up 21%), deal count: 4,719 (down 15%, eight-year low)

- Digital assets: $19.1B (nearly doubled)

- AI-focused fintech: $16.8B (up from $12.1B)

- B2B products: $13.5B (strongest since 2019)

- Payments: $19.2B (nine-year low in deal count)

- Wealthtech: $1.4B (down 71% from $4.9B record)

- Americas: $66.5B | EMEA: $29.2B | APAC: $9.3B (declining)

- VC: $56.7B across 3,765 deals | M&A: $55.4B across 840 deals

If you're building a company, this environment rewards category leaders and punishes the middle of the pack. If you're investing post-exit, the dispersion between good managers and bad managers matters more than the asset class label on the fund. The concentration dynamic isn't temporary. It's structural.

Tender Offers Are Quietly Replacing Traditional Exits

While the IPO pipeline builds and venture rounds get larger, a parallel liquidity system is growing fast enough to matter.

Decagon completed its first employee tender offer this week at a $4.5 billion valuation — a threefold increase from June. The company is less than three years old. The tender was led by the same investors who backed its $250 million Series D two months ago: Coatue, Index, a16z, Definition, Forerunner, and Ribbit.

Decagon isn't unusual. It's the latest example in a pattern that accelerated through 2025 and into early 2026.

TechCrunch reported on the structural shift: secondary sales have moved from founder-focused payouts (think the Hopin era, when founders took large personal positions off the table) to employee-wide tender offers designed primarily as retention tools. ElevenLabs authorised $100 million in employee secondary sales at a $6.6 billion valuation — double its previous round. Linear completed a tender offer at $1.25 billion. Clay ran two tender offers in nine months.

Why this matters for pre-exit founders:

These tender offers work because investors are eager to increase ownership in fast-growing AI companies. Buyer demand makes employee liquidity possible. If your company can attract that kind of investor appetite, structured tender offers become a legitimate retention tool — particularly when you're competing for engineering talent against companies that already offer them. The mechanics aren't trivial (409A implications, tender offer rules for 10+ sellers, board approval, tax structuring), but the playbook is increasingly well-established.

Nick Bunick, a partner at secondary-focused VC firm NewView Capital, told TechCrunch: "A little liquidity is healthy, and we've certainly seen that across the ecosystem."

Why this matters for post-exit founders allocating capital:

Tender offers are the buy side of the equation. When Coatue and a16z lead a tender offer at Decagon, they're not buying primary shares at IPO. They're acquiring secondary positions in a fast-growing private company at a price set between willing buyers and sellers. For founders with $20M+ in liquid capital looking for alternative deal flow beyond traditional fund allocations, tender offer participation through secondary-focused vehicles (like NewView, Forge, or CartaX) is a growing channel worth understanding.

The tension nobody's flagging:

One VC told TechCrunch something worth sitting with: tender offers "enable companies to stay private longer, reducing liquidity for venture investors, which is a challenge for LPs." In other words, tender offers solve the employee retention problem but may worsen the LP distribution problem we've covered for weeks. If companies can provide employee liquidity without going public, the pressure to IPO decreases. If IPOs decrease, LP distributions slow further. If distributions slow, LPs have less capital to commit to new funds.

Tender offers are good for employees. They may be quietly making the LP liquidity problem worse.

That's the kind of second-order effect that shows up in your portfolio twelve months after the headlines — particularly if you're invested in venture funds whose GPs are counting on IPO exits that now have a viable alternative.

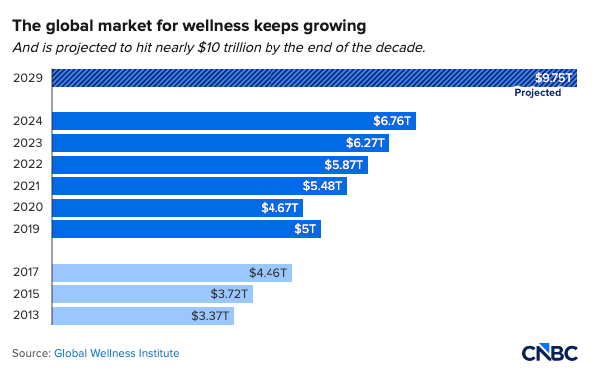

Quick Signal: The Longevity Economy Is Real. Here's Where It's Heading.

Equinox's $40,000-a-year "Optimize" membership has a waitlist of more than 1,000 people. A gym programme that costs more than many people's annual savings has a queue. The programme bundles personal training, nutrition coaching, sleep coaching, massage therapy, and a "health concierge," all structured around 100 biomarker tests twice a year through a partnership with Function Health.

The global wellness market is projected to reach nearly $10 trillion by 2030, up from $6.8 trillion in 2024, according to the Global Wellness Institute. Equinox's executive chairman, Harvey Spevak, said 2025 was a "record year" and expects 2026 to be bigger. Life Time launched a competing programme called Miora. Four Seasons now offers stem cell treatments and biomarker testing at select properties. The "gym as longevity clinic" model is replacing the gym as a status symbol.

This isn't about gym memberships. It's about where wealthy spending is migrating — from products to performance, from status objects to biological optimisation.

For post-exit founders, the longevity economy shows up in three places worth paying attention to:

As personal spending. Many founders describe a post-exit progression: first, you fix the portfolio, then you realise you've been neglecting your body through years of cortisol, poor sleep, and skipped checkups. The demand Equinox is seeing reflects real behaviour among the $5M–$100M cohort, not just billionaire biohacking.

As an investment category. Wellness infrastructure, diagnostic platforms, precision health, longevity-focused venture funds — institutional capital is entering. The $10T market projection isn't aspirational. Consumer spending is already there; the investment infrastructure is catching up. Specific areas attracting capital: biomarker testing companies (Function Health), personalised protocol platforms, and wellness-adjacent real estate (Equinox Hotels, Six Senses resorts).

As a portfolio allocation question. If you're building a family office-level investment framework, health and longevity are emerging as a distinct sector exposure rather than a subsector of biotech. The consumer behaviour data suggests durability. When wealthy individuals shift spending from watches to biomarkers, that's not a trend. That's a preference rewrite.

Until next time!