Nobody builds a company without a plan. Cap tables get structured before the first hire. Vesting schedules get negotiated before Series A. Operating agreements get lawyered before a single customer shows up.

But estate planning? The thing that determines what happens to everything you've built?

Most founders treat it like a problem for later. Later, when they're older. Later, when things are "settled." Later, when they finally have time.

Tony Hsieh had time. The Zappos founder sold to Amazon for $1.2 billion, had an estimated net worth of $840 million, and was 46 years old. Harvard-educated, surrounded by lawyers and advisors. He died in 2020 with no will, no trust, no estate plan of any kind.

Under the Nevada intestacy law, everything went to his parents. The federal estate tax exemption that year was $11.58 million. On an $840 million estate, that's a rounding error. The potential tax exposure ran into the hundreds of millions. Five years later, a will was actually found among the belongings of a friend who'd since developed dementia and died. It contained specific bequests: $50 million to trusts, $3 million to Harvard, and various charitable gifts. None of which were honoured during the initial distribution. A legal fight to reopen the entire estate is now underway.

This wasn't a matter of intelligence. He just never got around to it.

For first-generation wealth creators, estate planning carries a burden that inherited wealth doesn't face. There are no existing structures to build on. No family office with established trusts. No grandfather's lawyer who knows the history. Everything needs to be designed from scratch. For globally mobile founders with assets, businesses, and family across multiple countries, the number of things that can go wrong grows with each passport stamp.

What's Inside

- Default rules are expensive: US federal estate tax is 40% above the exemption. UK inheritance tax is 40% above £325,000. Japan tops out at 55%. Without deliberate structures, multiple jurisdictions may each claim a piece

- Common law vs. civil law changes everything: Common law jurisdictions allow testamentary freedom and recognise trusts. Civil law jurisdictions impose forced heirship rules and may not recognise trusts at all

- Inaction has a specific cost: Tony Hsieh died with $840M and no estate plan. Stieg Larsson's 32-year partner inherited nothing. Aretha Franklin's family spent five years in court. The Rockefellers, by contrast, have preserved wealth across six generations

- US exemption shifted the calculus: The OBBBA permanently set the federal exemption at $15M individual ($30M married) from January 2026, with no sunset. But state-level taxes and US citizenship-based worldwide taxation still apply

- Cross-border collisions destroy plans: Forced heirship can override a will. Double taxation hits without treaty coverage. Domicile, residence, and citizenship each trigger different obligations. Every jurisdiction needs its own analysis

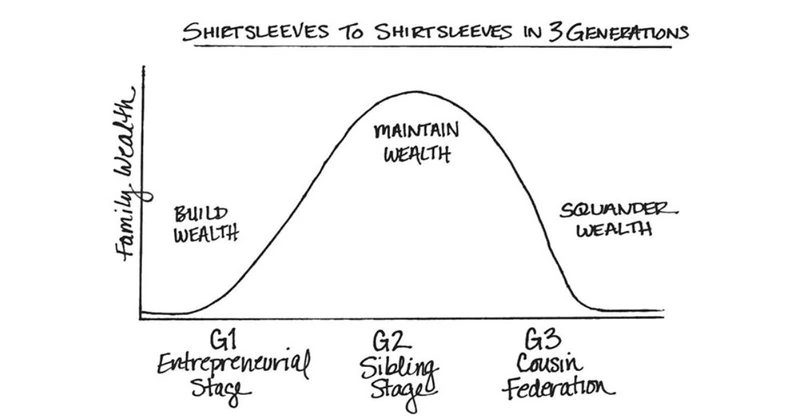

- Communication matters more than structure: 70% of wealthy families lose their wealth by the second generation, and 60% of those failures stem from communication breakdowns, not bad financial planning

Why This Matters Now, Even If You're 40 and Healthy

Estate planning isn't about death. It's about control.

Specifically, it's about maintaining control over three things: who gets what, when they get it, and how much the government takes in between. Without a deliberate structure, every jurisdiction where you hold assets will impose its own default rules. Those defaults rarely align with what a founder actually wants.

Numbers are stark. In the US, the federal estate tax rate is 40% on everything above the exemption threshold. The UK charges 40% above £325,000, a threshold that hasn't moved since 2009 and is now frozen until at least 2030. Japan's top inheritance tax rate hits 55%. South Korea takes 50%. France charges up to 45% for direct heirs and 60% for distant relatives.

A founder with £10M in UK assets and no estate plan faces roughly £9M in taxable value. The bill comes to £3.6M. One cheque to HMRC wipes out more than a third of what took a lifetime to build. And that's just one jurisdiction. Hold property in France, a business in the UK, and investments in the US, and three separate tax regimes may each claim a piece.

Williams Group conducted a 20-year study of over 3,200 wealthy families and found that 70% lost their wealth by the second generation, with 90% gone by the third. Only 3% of those failures were due to poor financial planning. 60% resulted from communication breakdowns and a lack of trust within the family. The structures weren't built. The conversations didn't happen. The default rules took over.

(Some researchers have questioned the methodology behind these figures. The original study focused on a single industry and region. But even if the precise percentages are debatable, the pattern holds: unstructured wealth transfers fail at alarming rates.)

Compare that to the Rockefeller family. Their 1934 Family Trust and 1952 Dynasty Trust have passed wealth to over 170 heirs across six generations. The family's combined net worth today is around $8.4 billion, built on a fortune amassed in the 1870s. What made it work wasn't just the legal architecture. It was the governance layer on top: professional trustees (originally Chase Bank, now JPMorgan), a formal family constitution, separate arms for investments, venture capital, insurance, and risk management. Irrevocable trusts funded by life insurance policies on each family member kept the structures continually replenished across generations. For founders interested in how that governance layer works in practice, the Running a Family Office Under $100M playbook covers operating models and decision structures in detail.

The Vanderbilts, by contrast, were America's wealthiest family in the same era. Within three generations, the fortune was functionally gone. No family constitution. No governance structure. No restrictions on distributions. Same starting conditions, radically different outcomes. The variable was planning.

What Are You Actually Optimising For?

Before choosing any structure, founders need to answer a question that doesn't have one right answer: what matters most?

Control is where most founders start. They want to keep their hands on the wheel, dictating who gets what, when they get it, and under what conditions. That instinct makes sense. You built this. Letting go doesn't come naturally.

Protection pulls in the opposite direction: shielding assets from creditors, divorce claims, lawsuits, or a 25-year-old heir who thinks crypto day-trading is a career plan. The more shielded assets are, the less accessible they become to you. A revocable trust gives you full control and flexibility but zero protection. An irrevocable trust delivers protection and tax benefits but limited flexibility. The trade-off is real and unavoidable.

Tax efficiency is the one everyone fixates on first, but it should be the third question, not the first. Minimising the government's cut at each transfer point matters, but only after control and protection are sorted. Different jurisdictions offer wildly different efficiency profiles, and what's optimal shifts with every budget cycle. The Tax Frameworks for Global Founders playbook maps how these jurisdictional differences compound for mobile founders.

Then there's flexibility, which people often forget. Your family at 45 looks nothing like your family at 65. Children grow up. Relationships evolve. Tax regimes change. A structure designed in 2026 might be completely wrong by 2036.

No single structure maximises all four simultaneously. A foundation in Liechtenstein offers flexibility and tax efficiency for certain profiles, but requires genuine substance and entails real ongoing costs.

Map your priorities before talking to lawyers. Otherwise, the structure you end up with will be convenient for the advisor to administer rather than one that actually fits your family's situation.

Common Law vs. Civil Law: Where Your Options Begin and End

The single most important factor in cross-border estate planning is whether a jurisdiction follows common law or civil law. This shapes everything that follows.

Common law jurisdictions (the US, UK, Australia, Canada, and most former British colonies) generally allow testamentary freedom. You can leave your assets to whoever you want. This system makes trusts work because common law recognises the split between legal ownership (the trustee) and beneficial ownership (the beneficiaries).

Civil law jurisdictions (most of continental Europe, Latin America, parts of Asia) operate differently. Many impose forced heirship rules: a fixed portion of your estate must pass to specific heirs, usually children, regardless of what your will says. France requires 50–75% for children, depending on the number of children. Italy limits free disposition to roughly one-third. Germany, Spain, Switzerland, Belgium, and Portugal all maintain similar rules.

What does this collision look like in practice? Consider Stieg Larsson, the Swedish author of The Girl with the Dragon Tattoo. He died unexpectedly in 2004 at age 50 with no will. He and his partner, Eva Gabrielsson, had been together for 32 years but had never married, partly for security reasons related to his investigative journalism on far-right extremist groups.

Under Swedish law, unmarried partners have no inheritance rights. Zero. Everything, including the royalties from a trilogy that would go on to sell over 100 million copies, went to his father and brother, relatives whom Gabrielsson says were largely estranged from his life. She received the apartment they'd shared and his personal effects through a settlement. Nothing else. Two decades of legal battles over his literary legacy followed.

One will, drafted by a Swedish lawyer, would have prevented it all.

For a founder who sold a tech company, moved to Portugal, owns property in France, holds investments through a UK structure, and has US citizenship, common law and civil law systems collide at every point. The US taxes worldwide assets based on citizenship. France applies forced heirship to property within its borders. Portugal applies its own succession rules. A UK trust might not even be recognised by the French notaire handling the estate.

EU Succession Regulation (Brussels IV), which entered into force in 2015, was supposed to simplify this. It allows EU residents to elect the law of their nationality to govern their entire succession. A British national living in France could, in theory, choose English law and its testamentary freedom to override French forced heirship.

In practice, the picture is more complicated. France passed legislation in 2021 allowing heirs who would have been "protected" under French law to claim compensation from French-situs assets, even when English law is elected. A German court ruled in 2022 that an election under English law was incompatible with German public policy when it completely disinherited a son with German nationality. The clean jurisdictional separation that Brussels IV promised is eroding case by case.

A structure valid in one jurisdiction cannot be assumed to work in another. Every country where you hold significant assets needs its own analysis, its own lawyer, its own will, its own understanding of local succession rules.

Everything here is free. Subscribing just tells me the content is useful — and helps me decide what to write next.

Trusts: The Workhorse of Common Law Estate Planning

A trust is a relationship where one person (the trustee) holds legal title to assets for the benefit of others (the beneficiaries), according to rules set by the person who created it (the settlor). The variations within this single concept are enormous.

Revocable trusts (primarily in the US) allow the settlor to retain full control. Change beneficiaries, move assets, or dissolve it entirely. They're useful for avoiding probate and maintaining privacy, but they offer neither asset protection nor tax benefits. The IRS treats assets in a revocable trust as still belonging to you. Aretha Franklin's case shows why even basic estate planning matters: she died in 2018 with an estimated $80 million estate and no proper estate plan. Two handwritten wills were found, one under a couch cushion, another in a locked cabinet, with conflicting instructions. Her four sons spent five years in court fighting over which scribbled document represented her wishes. Her lawyer, with whom she'd worked for nearly three decades, told NBC he'd repeatedly urged her to set up a formal will and trust. She never did. A revocable trust would have kept the entire thing out of court and out of the press.

Irrevocable trusts are where real planning happens. Once assets go in, they're generally out of your estate for tax purposes. You give up control in exchange for protection and efficiency. Within this category, the options run deep: GRATs (Grantor Retained Annuity Trusts) transfer appreciation while the settlor retains income. IDGTs (Intentionally Defective Grantor Trusts) allow sales to the trust without recognising capital gains. SLATs (Spousal Lifetime Access Trusts) let married couples lock in exemptions while maintaining indirect spousal access.

Discretionary trusts give the trustee broad authority to decide who receives what and when. They're the most flexible form and the most common in the UK and offshore planning. The trustee, guided by a non-binding letter of wishes, allocates income and capital among a class of beneficiaries based on changing circumstances. For families where it's not yet clear who will need what, this is usually the right starting point.

Purpose trusts exist in certain offshore jurisdictions and can hold assets for a specific objective rather than named beneficiaries. Primarily commercial and charitable, but they occasionally feature in complex wealth structures.

Protector role matters more than most founders realise. In jurisdictions that allow it, a protector sits alongside the trustee with specific reserved powers: the ability to change trustees, veto distributions, or amend trust terms within defined limits. For a founder who struggles to let go of control (and that's most of them), the protector role offers a structured middle ground between running everything and trusting a stranger with your family's wealth.

US-Specific Structures: What the New Exemption Means

The US estate tax picture shifted permanently in 2025. The One Big Beautiful Bill Act set the federal estate and gift tax exemption at $15 million per individual, or $30 million for married couples, starting January 1, 2026. Unlike the previous TCJA provision, this has no sunset date and will be indexed for inflation going forward.

For founders in the $5M–$30M range, this changes the calculus considerably. A married couple with $30M or less in combined assets now faces zero federal estate tax. That doesn't make estate planning unnecessary. State-level estate taxes in places like Massachusetts (which taxes estates above $2M), Oregon, and New York still apply at much lower thresholds. And the 40% federal rate on amounts above the exemption remains severe for larger estates.

Dynasty trusts, available in states like South Dakota, Nevada, and Alaska, hold assets for multiple generations, potentially in perpetuity, without triggering generation-skipping transfer tax at each level. South Dakota has become the jurisdiction of choice because it combines no state income tax, perpetual trust duration, and strong asset protection statutes. The Rockefellers pioneered this approach. Modern founders are replicating it on a smaller scale. For a broader look at how location decisions interact with wealth structures, see the Family Office Location Guide.

Grantor trusts remain highly tax-efficient. Because the grantor pays income tax on trust earnings personally, the trust grows tax-free while the grantor's taxable estate shrinks by the amount of tax paid. It's essentially an extra gift that doesn't count against the exemption.

For US citizens living abroad, the picture gets more complicated. The US taxes worldwide assets based on citizenship, not residence. Moving to Portugal or the UAE doesn't remove US estate tax obligations. And foreign trusts with US beneficiaries or US settlors trigger onerous reporting requirements (Forms 3520 and 3520-A), with penalties for non-compliance that can reach 35% of the trust's assets. That's not a typo. 55% for a reporting failure.

UK-Specific Structures: IHT and the Rise of Family Investment Companies

The UK inheritance tax regime is, by most objective measures, more aggressive than the US system for wealthy individuals. The nil-rate band has been frozen at £325,000 since 2009. The government has confirmed it won't budge until at least 2030-31. Combined with the residence nil-rate band of £175,000 (only available when a home passes to direct descendants), a married couple can shield up to £1 million. Everything above that: 40%.

A founder with a £10M estate is looking at roughly £3.6M in inheritance tax. More than a third of the estate, gone in a single transfer. For someone who spent a decade building a company, that number tends to focus the mind.

The traditional UK planning tool, the discretionary trust, has become less attractive since 2006, when the government introduced periodic charges of up to 6% every ten years and exit charges when assets leave the trust. For large wealth, those ongoing charges erode the benefit significantly.

Family Investment Companies (FICs) have emerged as a compelling alternative. An FIC is a private company where family members hold different classes of shares. Typically, the founders retain voting shares (with no rights to capital growth), while children hold growth shares (with no voting power). HMRC investigated FICs in 2019, found no evidence of non-compliance, and folded the investigation unit in 2021. That's about as close to a green light as UK tax authorities ever give.

Founder transfers cash into the FIC (often structured as a loan that stays in the estate and can be repaid tax-free over time). Growth shares are gifted to family members as potentially exempt transfers (PETs). If the founder survives for seven years, those shares are entirely excluded from the estate for IHT purposes. Meanwhile, investment income within the FIC is taxed at corporation tax rates (currently 19–25%) rather than the individual's marginal rate of up to 45%.

Seven-year clock on PETs is one of those things that sounds like plenty of time until you realise you should have started it five years ago. Every year that passes reduces the IHT exposure through taper relief. Planning early isn't optional. It's the mechanism that makes the whole structure work.

Business Property Relief also deserves attention in this context. It has historically offered 100% IHT relief on qualifying trading business assets, but from April 2026, it's being capped at £1 million, with a reduced 50% relief rate above that threshold. Founders still holding operating businesses need to revisit their plans.

Offshore Structures: When They Make Sense (and When They Don't)

I'll say something most wealth advisors won't: offshore structures get disproportionate attention relative to how many founders actually need them.

For someone with $5M–$20M in assets, a single residence, and a family in one country, the costs and complexity of an offshore trust rarely justify the benefits. The setup runs $20,000–$75,000. Annual administration costs $15,000–$50,000 or more. Add the professional fees for ongoing compliance across multiple jurisdictions, and you need meaningful tax savings just to break even.

Where offshore planning becomes genuinely useful is when multiple jurisdictions are already in play. A founder holding UK property, US investments, and Dubai residency, with family members tax-resident in different countries, faces coordination problems that domestic structures alone can't solve. An offshore trust in Jersey, Guernsey, or the Cayman Islands can serve as a neutral holding vehicle that sits above the jurisdictional conflicts.

Substance requirements have tightened significantly. The EU's anti-tax avoidance directives, CRS automatic information exchange, and individual country enforcement mean that a brass-plate structure with no real activity will attract scrutiny. Any offshore arrangement needs real trustees, real administration, and real decision-making in the chosen jurisdiction. The days of a name on a door in the Channel Islands are over.

Run the numbers honestly. If the tax savings don't clearly exceed setup costs, running costs, and the compliance overhead, the complexity isn't worth it. There are enough expensive mistakes to make in estate planning without adding unnecessary layers.

Foundations: The Civil Law Alternative

For founders with connections to civil law jurisdictions, foundations offer something trusts can't easily replicate.

A private foundation is a legal entity, not a relationship like a trust, that holds assets in its own name. The founder establishes the foundation with a charter defining its purpose, governance, and beneficiary rules. It owns its assets directly, rather than splitting legal and beneficial ownership the way a trust does.

Liechtenstein, the Netherlands, and Panama are the most commonly used jurisdictions. Liechtenstein foundations are flexible and internationally well-recognised. Panama foundations are popular with Latin American families because civil law courts in the region recognise them readily, and costs are relatively low.

Key distinction: civil law courts that refuse to recognise trusts (because split legal and beneficial ownership doesn't exist in their system) will often recognise a foundation as a legal entity. For founders with assets in France, Germany, Italy, or Spain, this can be the difference between a structure that survives a legal challenge and one that gets dismantled by a local court.

Cross-Border Complications: Where Millions Get Lost

The most expensive mistakes in international estate planning come from assuming one country's rules apply everywhere.

Forced heirship vs. testamentary freedom. A will drafted in London giving everything to a spouse may be completely invalid in France, where children have an automatic right to a share. Larsson's case in Sweden is the extreme version. But milder collisions happen constantly. A founder assumes their English law will cover the apartment in Barcelona, and it doesn't. Property physically located in a forced heirship jurisdiction is especially vulnerable, even with a Brussels IV election.

Double taxation. Without treaty protection, the same asset gets taxed twice: once by the country where it's located, and again by the country of the owner's domicile or citizenship. The US has estate tax treaties with roughly 15 countries, and gift tax treaties with seven. The UK has a handful of its own. Outside these treaty networks, double taxation is a real risk that requires careful credit planning.

Trust recognition. Several civil law jurisdictions don't recognise trusts, or recognise them only partially under the Hague Trust Convention. If assets are held in a trust but located in a non-recognising country, local courts may treat the assets as belonging to the settlor or the trustee, resulting in entirely different tax consequences than intended. This is where foundations have a structural advantage.

Domicile vs. residence vs. citizenship. These three concepts carry different tax implications, and they don't always line up. The UK has been taxing based on domicile, though it's shifting to a residence-based system from April 2025 for individuals who have been resident in the UK for 10+ years of the last 20 years. The US taxes based on citizenship. Many European countries tax based on residence. A founder who is a US citizen, UK-domiciled, and UAE-resident needs to work across all three frameworks simultaneously, and the advisors in each jurisdiction need to coordinate.

Integration With Business Structures

An estate plan and a holding structure can't be designed in isolation. They need to work together.

Common pattern for post-exit founders: hold liquid investments through a holding company, with the holding company shares owned by a trust or FIC. This creates a clean separation between the investment management layer and the succession layer. The holding company can sit in a tax-efficient jurisdiction, while the trust or FIC handles inheritance and distribution.

For founders still holding operating businesses, succession planning and estate planning overlap significantly. Business Property Relief in the UK (100% relief on qualifying trading business assets for IHT, though capped at £1M from April 2026 with a 20% reduced rate above) can dramatically reduce the tax bill, but only if the business genuinely qualifies and the ownership structure is set up correctly.

In the US, valuation discounts on minority interests in family-held businesses remain powerful. Transferring a minority interest in a family LLC to a trust at a discounted valuation allows more wealth to move within the gift tax exemption than the underlying asset values would suggest. It's one of the more effective tools available, and it's entirely legal, but it requires proper appraisal documentation.

The Documentation You Actually Need

Powers of attorney sound boring until someone is trying to sell a property in Spain from a hospital bed in London, and nobody has the legal authority to sign.

At a minimum, every founder with $5M or more needs:

Will in every jurisdiction where you hold significant immovable assets. A UK will for UK property. A French will for French property. Each is drafted by a local lawyer who understands both local succession law and cross-border interactions. A French will that inadvertently revokes the UK will creates chaos. It happens more often than you'd think.

Lasting powers of attorney (or local equivalents) in each relevant jurisdiction. A UK LPA doesn't automatically work in Spain. Each country needs its own instrument, properly executed in accordance with local rules.

Letters of wishes for any trusts or FICs. Not legally binding, but they guide trustees on your intentions. Update them regularly. A letter of wishes from 2018 reflecting a family situation that no longer exists helps nobody.

Clear record of all structures, accounts, and advisors. One secure document mapping every entity, every account, every key contact. This prevents weeks of expensive professional reconstruction when something goes wrong. The Hsieh case is the cautionary tale here: his family didn't even know what he owned, let alone how it was structured.

Business succession documentation if operating businesses is still held: buy-sell agreements, shareholder agreements, and key person insurance where relevant.

When to Involve Family

This is where the Williams Group data cuts deepest. Their research found that 64% of wealthy parents have disclosed little to nothing about their wealth to their children. The instinct to protect children from the burden of knowing about family wealth is understandable. It's also the single biggest predictor of wealth transfer failure.

The tension is real. Too much transparency too early can create entitlement or reduce motivation. Too little transparency leaves heirs unprepared for responsibilities they didn't ask for and don't understand. As a Kiplinger analysis noted, silence doesn't prevent entitlement; it prevents preparation.

Approach that tends to work involves graduated disclosure: sharing values and principles early, introducing structural concepts in the teenage years, involving adult children in governance discussions, and disclosing specific numbers only when heirs demonstrate financial literacy and emotional readiness. The Governance and Decisions chapter of the Family Office playbook covers the mechanics of formalising these conversations.

For founders transitioning into Owner Mode, designing structures and incentives rather than running day-to-day operations, involving the family in estate governance is a natural extension. The same skills that make someone effective at designing company governance (clear decision rights, defined roles, transparent reporting) apply directly to family wealth governance. Most founders just don't make the connection until someone points it out.

Where to Start

Estate planning at this level is complex enough that doing it alone is not realistic. But founders who walk into their first meeting with an estate planning lawyer cold, with no framework for what they want, tend to end up with structures that serve the advisor's preferences rather than the family's needs. A UK solicitor will default to a discretionary trust. A US attorney will suggest an irrevocable trust. Neither is wrong, but neither is necessarily asking the cross-border questions that actually matter.

Founders who get the most from these conversations tend to arrive with their priorities already mapped out. Are they optimising primarily for control, protection, tax efficiency, or flexibility? What's the realistic timeline: 40 with decades ahead, or 60 with urgency? How many jurisdictions are genuinely in play? Is there a succession plan for any operating businesses?

Then comes the documentation audit. Valid wills in every relevant jurisdiction? Powers of attorney? Do existing structures actually reflect the current situation and intentions, or do they reflect a life from five years ago?

Cross-border estate planning requires coordination among tax advisors, estate planning lawyers, and, in some cases, trust companies across multiple jurisdictions. The biggest risk isn't choosing the wrong structure. It's having advisors in different countries who don't talk to each other.

Founders who preserve wealth across generations aren't the ones with the cleverest structures. They're the ones who started the boring work early, built the governance to match, and kept reviewing it long after the initial urgency faded.

This is educational content. Your situation requires professional advice tailored to your specific circumstances.

Frequently Asked Questions

Do I need a separate will for every country where I own property?

For immovable assets (real estate), yes. In most cases, you need a will governed by local law in each jurisdiction where you hold property. This is because many countries apply their own succession rules to real estate within their borders, regardless of where you live or what your "main" will says. Each will should be drafted by a local lawyer who understands both local succession rules and how the will interacts with your wills in other jurisdictions. A French will that inadvertently revokes a UK will is a common and expensive mistake.

What is a dynasty trust, and who should consider one?

Dynasty trust is a long-duration (potentially perpetual) trust structure that holds assets across multiple generations without triggering estate or generation-skipping transfer tax at each generational transfer. In the US, states like South Dakota, Nevada, and Alaska allow trusts to last indefinitely. They're most relevant for founders with estates well above the federal exemption ($15M for individuals / $30M for married couples as of 2026) who want to preserve wealth across generations. Below that threshold, simpler structures usually suffice.

How do forced heirship rules affect my estate plan?

If you hold assets in a civil law jurisdiction (France, Germany, Italy, Spain, and most of continental Europe), local law may require a fixed portion of your estate to pass to specific heirs, usually children, regardless of what your will says. This can override the provisions of a trust or will drafted under common law. The EU Succession Regulation (Brussels IV) allows some flexibility through nationality elections, but recent court decisions in France and Germany have weakened these protections. Any assets in forced heirship jurisdictions need specific local planning.

What happens if a US citizen dies abroad without an estate plan?

US taxes worldwide assets based on citizenship. If a US citizen dies intestate (without a will) abroad, their US assets are distributed under the intestacy laws of their last US state of domicile, while foreign assets may be subject to local succession rules. The estate could face US federal estate tax, potentially a state-level estate tax, and foreign inheritance or succession taxes, with limited treaty relief. Double taxation is a real risk. Foreign trusts with US connections also trigger severe reporting penalties for non-compliance (up to 35% of trust assets).

What is a Family Investment Company, and why are they popular in the UK?

Family Investment Company is a private limited company where the founder retains voting control through one class of shares, while growth shares are held by (or gifted to) family members. Investment income is taxed at corporation tax rates (19–25%) rather than personal rates (up to 45%). Growth shares gifted as potentially exempt transfers fall outside the estate for IHT if the founder survives seven years. HMRC investigated FICs in 2019, found no compliance issues, and closed the investigation unit in 2021.

How much does cross-border estate planning typically cost?

Costs vary significantly based on complexity. A single-jurisdiction plan with a standard trust or will might cost £5,000–£20,000 in professional fees. Cross-border planning involving two or three jurisdictions typically runs £30,000–£75,000 in setup costs, with annual administration and compliance costs of £15,000–£50,000 or more. Offshore structures add further expense. The relevant question isn't whether it's expensive, but whether the cost of planning is less than the cost of not planning, which, for estates above $5M, it almost always is.

Capital Founders OS is an educational platform for founders with $5M–$100M in assets. Frameworks for thinking about wealth — so you can make better decisions.

Explore more: Playbooks · Capital Signals · Wealth Architecture · Investment Strategy · Business Building · Life Design

Found this useful? Forward it to a founder who's thinking about this stuff. Got a question or disagree with something? Get in touch.

New here? Subscribe for one email a week.