Understanding advisers, managers, custodians, and where conflicts of interest hide. A practical guide for founders managing $5M–$100M in liquid assets.

Before you invest seriously, you need to understand how the investment world actually works. Not the textbook version. The real one — with real incentives, real conflicts, and real costs for getting it wrong.

I work in wealth management. I've watched smart people make expensive mistakes because they sat in meetings nodding along, too embarrassed to ask questions. They had no idea what was happening to their money. Some of them had eight-figure portfolios.

Know the landscape before you deploy capital into it.

What You'll Learn

- 92% of advisers charge AUM fees — the median is 1% on $1M portfolios, but 62% charge at least that while only 32% do at $2M. Fee negotiation matters as you scale

- Even Vanguard got caught: paid $19.5M to settle SEC charges for hiding adviser incentives — commission-based conflicts aren't limited to shady firms

- Emerging market commissions run 5–7% on structured products vs. 2% in the UK — that difference comes directly out of your returns

- BNY holds $52.1 trillion in custody — larger than the GDP of the US, China, and Japan combined. Know where your assets actually sit in the custodian chain

- Retail vs. accredited isn't binary: you can keep retail protections for core holdings while opting into accredited status for specific opportunities

- Four questions for any adviser: Do you receive commissions? Are fees tiered? What's hidden? Are you a fiduciary?

Scale of the Game

PwC's 2025 Global Asset & Wealth Management Report puts global assets under management at $139 trillion in 2024, projected to reach $200 trillion by 2030. Total investable wealth worldwide should exceed $481 trillion by decade's end.

That $139 trillion shapes every market you'll take part in. It comes from two sources. Big pools of money — pension funds, insurance firms, endowments, and sovereign wealth funds — invest to meet long-term obligations, such as paying pensions and claims. The rest is private wealth: money owned by people.

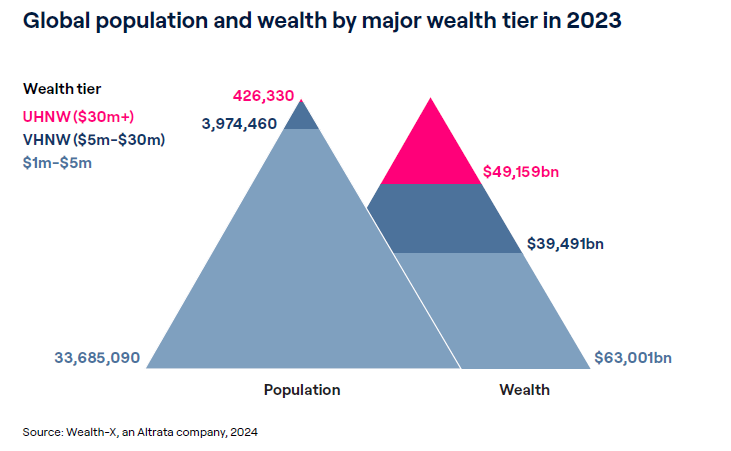

Altrata's World Ultra Wealth Report 2024 counted 38.1 million people globally with at least $1 million in assets. Of those, 426,330 have over $30 million. Together, they control $49.2 trillion — more than the combined GDP of the US and China.

UBS's 2025 Global Wealth Report tracks a segment they call "EMILLIs": everyday millionaires with $1–5 million. Their numbers have quadrupled since 2000. There are now 52 million of them, holding $107 trillion.

Family offices are growing fast, too. Deloitte counted 8,030 single-family offices around the world in 2024, up 31% from 2019. They expect 10,720 by 2030. The wealth behind them jumped from $3.3 trillion to $5.5 trillion in just five years.

From here, we focus on private wealth and the players who manage it. Or, in some cases, to skim from the people who own it.

Managing It Yourself vs. Getting Help

Some founders run their own money. They read annual reports at night, check futures before coffee, and enjoy the process. If your setup is simple — liquid assets, one country, no big stock positions — a mix of low-cost index funds and some discipline can work.

Complex setups change that. When you're dealing with several countries, a large stockholding from a recent exit, entities in different places, and estate planning across borders, mistakes can be costly. Not because founders lack brains, but because the links between tax, structure, and investing create traps that aren't clear until something breaks.

The honest take: simple money is easy to manage. Complex wealth needs help, and the cost of bad choices usually exceeds the cost of good advice. For a deeper look at how to think about investment strategies and which ones fit different goals, that's covered elsewhere.

Retail vs. Accredited Investors

Regardless of approach, every investor gets put into one of two buckets.

Retail investors get strong legal shields but can't access products like hedge funds and private equity. This is the default. Even with $100 million.

Accredited investors get broader access. More choices, higher upside, higher risk, fewer guards.

In the US, you qualify through income ($200,000+ a year, or $300,000 jointly), net worth ($1 million+ minus your home), or pro credentials like Series 7, 65, or 82.

What most people miss: these labels aren't fixed or all-or-nothing. You can stay retail for your core holdings — keeping the legal shields — while opting into accredited status for specific deals. Founders who just exited often benefit from this hybrid setup, keeping the bulk of their wealth protected while tapping into private market deals one at a time.

What Wealth Advisers Actually Do

Different advisers serve different wealth levels, and the cutoffs reflect real gaps in what's needed.

Under $3M usually means IFAs in the UK or RIAs in the US. Between $3M and $30M, wealth firms or private banks are the main options. From $30M to $100M, multi-family or virtual family offices start to make sense. For clients above $100M, single-family offices offer full in-house control. That said, founders with less than $100M can still run a family office if they want to be hands-on with how their wealth is managed.

These are rules of thumb, not hard lines. They map to economies of scale and the fact that a $5M pool and a $50M pool have very different needs.

A good adviser builds a plan for how to invest and spread your assets, helps with tax and structure, opens doors to deals you can't access alone, and helps guard what you've built. The adviser helps you set up the right structure, keep things balanced, and shift when the world changes.

How Advisers Get Paid — and Where Conflicts Hide

According to the 2024 Kitces Report, 92% of financial advisors use an assets under management (AUM) fee structure. The median is about 1% on portfolios up to $1 million, declining for larger balances.

Among advisors surveyed, 62% charge at least 1% on $1M portfolios. That drops to 32% for $2M portfolios. At higher wealth levels, some charge as low as 0.25% for portfolios of $100 million or more.

The fee schedule alone doesn't tell you much about where the real conflicts are.

Some advisers get paid by product makers — insurance firms, fund houses, platform providers. This isn't always shady, but the money trail matters. In mature markets, most advisers are paid by clients. In emerging markets, product firms pay the adviser. And the numbers are big: a structured product might pay 2% in the UK but 5% to 7% in other parts of the world.

That gap means your adviser may be drawn to products that pay well rather than products that work well for you. A World Economic Forum study was blunt: commission-based arrangements undermine what's best for investors.

You might think this only happens at small or poorly run firms.

Vanguard — built on the idea of putting investors first — paid $19.5 million to settle SEC charges for hiding conflicts. Their "salaried" staff were getting bonuses to push clients toward certain products. What the ads said and what the pay stubs said were two different things. SEC cases hit 200 in Q1 of fiscal 2025. The most since 2000.

If Vanguard can't keep its house clean, what does that tell you about the rest?

Four things to ask any adviser before handing over a dollar:

Do you receive commissions or referral fees from any products you recommend? What percentage do you charge on assets, and is it tiered as the portfolio grows? Are there hidden costs — transaction fees, platform fees, fund-level charges that don't appear in your headline fee? Are you a fiduciary, legally bound to act in my best interest?

Choosing an independent adviser paid exclusively by you helps. It doesn't eliminate conflicts entirely, but it removes the worst structural incentives.

Investment Managers

Once the plan is set, someone has to run it day to day.

Model portfolios serve most retail investors. They come in risk grades from cautious to bold, with low fees 0.1% to 0.5% a year. Custom portfolios, open to clients with $5 million or more, can hold hedge funds, private equity, and venture deals. Fees run up to 1% a year. Alternatives often carry the "2 and 20" model: a 2% annual fee plus 20% of profits above a hurdle rate.

The goals differ. Long-term portfolios use buy-and-hold with stocks, bonds, and ETFs. They track indices like the S&P 500, aiming to grow through market cycles.

Absolute return funds aim to make money regardless of market conditions. Hedge funds are the main vehicles for short selling, derivatives, and arbitrage. They don't measure against a benchmark. The only test is whether they made money.

Both types can live in one portfolio. The split matters because it shapes how you judge results. Grading a hedge fund against the S&P 500 is like scoring a goalie by how many goals they net.

Fund Managers vs. Portfolio Managers

This trips people up because both get called "asset managers."

Fund managers run single funds — hedge funds, PE funds, venture funds. These are building blocks. Portfolio managers put together and watch over your total mix using those blocks, whether third-party or in-house.

Big firms like Goldman Sachs, JPMorgan, and UBS do both. One arm runs funds. Another advises clients and builds portfolios. They also have private banks, trading desks, and brokerages under the same roof.

This breeds conflicts. When the same firm makes the products and picks them for you, the urge to push in-house funds is baked into the model. A Deloitte case study laid out the problem: one firm's advisors put roughly 50% of client money into their own funds. They chose pricier share classes of their own products while looking at cheaper options from rivals. More revenue for the firm. More cost for clients. None of it was disclosed.

The range of products on offer is vast: single assets (stocks, bonds, options, futures), pooled vehicles (mutual funds, ETFs, trusts), alternatives (hedge funds, PE, venture, real estate, crypto), and non-standard products (managed certificates, structured notes, ETNs).

Custody: Where Your Assets Actually Sit

Nobody thinks about custody until something goes wrong. And when custody goes wrong, everything goes wrong.

Custodians hold your assets. They keep your holdings apart from their own balance sheet, settle trades, collect dividends, handle stock splits, and meet all the legal rules.

In October 2024, BNY became the first bank to cross $50 trillion in assets under custody. They hit $52.1 trillion — larger than the GDP of the US, China, and Japan combined. The firm dates to 1784. Alexander Hamilton helped start it. State Street follows with $44.3 trillion. JPMorgan and Citi round out the "big four."

Holding client money is the most tightly watched business in finance. Custody is the fortress.

Smaller firms that hold client assets are usually sub-custodians. They have accounts at the giants. Your money may sit with a boutique, but somewhere up the chain, it's held at BNY or State Street. Knowing where your assets actually live — and how many layers sit between you and the custodian — matters more than most founders grasp.

In the US, retail investors typically have custody at Charles Schwab, Fidelity, Pershing, LPL Financial, or Altruist. In the UK, investment platforms like Aviva, Standard Life, Quilter, AJ Bell, and JustFA serve this function.

Custodians charge 0.10% to 0.30% on assets they hold, plus costs for reporting, corporate actions, and trades. Your statements should break down every fee. Read them. Fees stack up against your returns over decades.

Managed Accounts

Managed accounts split custody from the people making trades — and this split is one of the best shields you can have.

You keep assets with a large custodian (UBS, Goldman Sachs, Interactive Brokers) while outside advisers run the money in your account. The key: advisers can buy and sell for you, but cannot move funds out. This guards against the worst case — an adviser walking off with client money.

In Switzerland, this model is known as External Asset Management (EAM). Clients use private banks to hold assets and borrow, but hire outside advisers to manage portfolios and run investment strategies. It keeps two jobs apart that are often bundled elsewhere — sometimes with bad results.

The setup works for all sides. Clients stay safe with large banks. Banks earn custody fees. Advisers focus on picks and planning. For founders with a large stock position from a recent exit, this split adds a real layer of safety during the shift from running a business to managing cash.

Market Infrastructure

Behind every trade, behind every statement, a vast machine runs out of sight.

Banks handle new stock listings, M&A deals, and research. Brokers and prime brokers facilitate trades and lend to large clients. Exchanges and market makers create the places where buyers meet sellers. The SEC, FCA, and their peers set the rules. Clearing houses make sure trades settle cleanly. Data firms like Bloomberg and FactSet supply the tools.

You don't need to know every player in detail. Knowing they exist — and that each one runs on its own business model with its own motives — helps explain why markets act the way they do.

The System Behind the Portfolio

The world of investing has five layers:

Wealth owners — the people and groups with money to put to work.

Wealth advisers — the pros who help shape a plan and carry it out.

Fund and portfolio managers — the people who run funds and build your overall mix.

Custodians — the banks that hold and guard assets.

The plumbing — trading desks, exchanges, clearing houses, watchdogs, and data firms that keep the whole thing running.

Every fee, every conflict, and every risk hides in the gaps between these layers. Founders who treat their wealth as a system — rather than a pile of holdings — tend to build more durable setups and dodge the costly errors that come from trusting a machine you don't understand.

Get the system right. The picks and returns follow from there.

Capital Founders OS is an educational platform for founders with $5M–$100M in assets. Frameworks for thinking about wealth — so you can make better decisions.

Explore more: Playbooks · Capital Signals · Wealth Architecture · Investment Strategy · Business Building · Life Design

Found this useful? Forward it to a founder who's thinking about this stuff. Got a question or disagree with something? Get in touch.

New here? Subscribe for one email a week.