With $5 million to invest (or $50 million, or more) you've probably noticed something.

The most interesting opportunities don't appear on Bloomberg terminals. They're not in your private bank's quarterly model portfolio. They're not advertised on platforms with slick interfaces and one-click investing.

They're private. And for most investors, they're invisible.

Private equity has become essential infrastructure for serious capital. Not speculation. Not diversification for its own sake. Infrastructure. Something happened recently that makes this clearer than ever: according to Deloitte's 2024 Global Family Office Report, private equity has officially surpassed public equity as the dominant asset class in family office portfolios. PE now represents 30% of the average family office allocation, up from 22% in 2021. Public equities have dropped to 25%.

That's not a trend. It's a structural reallocation.

But what most people don't realise: getting access takes more than capital. You need relationships. You need a process. And you need to understand what you're actually signing up for — including how the broader investment landscape shapes which opportunities reach you in the first place.

What's Inside

- PE now dominates family office portfolios: 30% average allocation, surpassing public equities at 25% (Deloitte 2024). Over rolling 10-year periods, PE has outperformed public markets by 3%+ annually 68% of the time since 1992 — rising to 94% from 1999

- Manager selection is everything: Return dispersion between top and bottom quartile PE funds runs 1,000–1,500 basis points — compared to just 200 bps in public large-cap equity. Picking the right GP matters more than any other decision

- Club deals are the default structure: 60% of family office PE transactions are now club deals (PwC 2024). They offer scale without concentration, multiply expertise across partners, and provide full transparency — no fund overhead, no blind pools

- Exit timelines have stretched significantly: Average buyout holding periods hit 6.7 years, up from a two-decade average of 5.7 (McKinsey 2025). The exit backlog is the largest since 2005

- QSBS became more powerful in 2025: The One Big Beautiful Bill Act raised the exclusion cap to $15M per issuer and the gross asset threshold to $75M. At full exclusion, that's roughly $3.6M in federal tax savings

- Private credit complements PE — but with caveats: Senior direct lending offers 500–650 bps over base rates with shorter duration (3-5 years vs 7-10). But recent redemption halts and market dislocations mean rigorous manager diligence matters here too

- Access beats alpha: Quality deal flow is a function of reputation and relationships built over years, not capital alone. Start with 1-2 sectors where you have genuine expertise and build systematically

- Geographic diversification matters: Europe shows more stable PE outperformance versus public markets than the US. Asia-Pacific return dispersion is widening — top-quartile 2017 vintage funds delivered 25%+ IRR while bottom-quartile barely reached high single digits

Why Serious Capital Keeps Moving into Private Markets

The obvious question first. Why bother with all the complexity?

Returns

Cambridge Associates tracks private equity performance more rigorously than anyone. Their data covering over 1,600 US PE funds shows some patterns worth understanding.

In 2024, the Cambridge Associates US Private Equity Index returned 8.1%, while the Venture Capital Index delivered 6.2%. Not spectacular, but solid. More revealing is the long-term data: over rolling 10-year periods, private equity has outperformed public equities by 3% or more annually 68% of the time since 1992. That figure rises to 94% when you start counting from 1999.

These are net-of-fee numbers. After the managers take their 2% management fee and 20% carry.

But averages are dangerous in private markets. Return dispersion between top-quartile and bottom-quartile buyout funds runs around 14% in any given vintage year. For venture and growth equity, that gap stretches to 18%. Your experience depends almost entirely on which funds (or deals) you access.

That's actually the point. Private equity isn't a market you buy. It's a game where selection and access determine everything. If you're still working from the traditional balanced portfolio model, PE is where the gap between theory and practice widens.

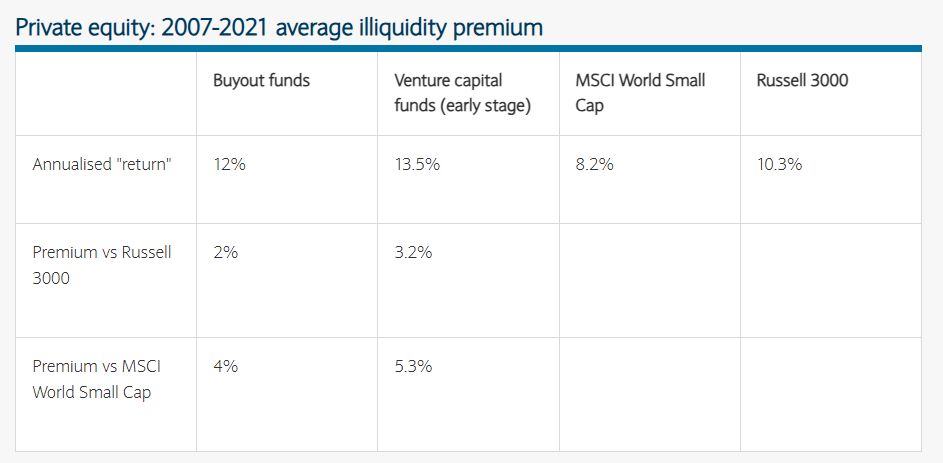

Illiquidity Premium (With a Reality Check)

You've heard the argument: you get paid extra for locking up your capital. Research from Barclays suggests the illiquidity premium runs 2-4% annually for buyout funds and 3-5% for venture capital.

The reality check nobody mentions: not every illiquid investment actually captures that premium. It depends entirely on entry price, deal structure, and timing. Simply tying up capital for seven years doesn't magically create alpha. You have to buy well.

And there's another dimension. Academic research shows that PE's perceived lower volatility is partly an artifact of appraisal-based valuations that smooth returns. The underlying businesses carry risks that public equity investors price immediately but PE investors discover on a lag. Something to remember when the quarterly statements look more stable than your public portfolio.

Tax Efficiency That Actually Moves the Needle

This is where private equity gets interesting beyond headline returns.

Done right, PE can be remarkably tax-efficient. The Qualified Small Business Stock (QSBS) exemption under Section 1202 is the biggest tool in the kit. It allows you to exclude capital gains from federal tax entirely on qualifying investments.

What changed recently: the One Big Beautiful Bill Act, signed in July 2025, made QSBS significantly more attractive:

- The exclusion cap increased from $10 million to $15 million per issuer (indexed for inflation starting 2027)

- The gross asset threshold for qualifying corporations rose from $50 million to $75 million

- A new tiered holding period means you can now get partial benefits earlier: 50% exclusion after 3 years, 75% after 4 years, and 100% after 5 years

At full exclusion, $15 million in capital gains becomes completely federal tax-free. That's roughly $3.6 million in tax savings at the top rate. Not trivial.

Beyond QSBS, there's the step-up in basis at death. PE holdings can reset their cost basis when passed to heirs, eliminating unrealised gains from a tax perspective. And the right structures (family partnerships, trusts, carried interest arrangements) can shift substantial value without triggering gift taxes. For founders thinking about how tax structures interact with jurisdictional choices, PE adds another layer of planning opportunity.

Private equity isn't just about chasing returns. For many families, a significant portion of the real return comes from effective structuring and tax management.

Three Paths into Private Equity

Not all private equity looks the same, and there are different ways to build exposure.

Traditional Fund Investing

The classic route. You commit capital as a Limited Partner (LP) to a fund managed by a General Partner (GP).

What works: Professional management. Diversified exposure across 15-25 portfolio companies. Access to institutional-quality deal flow you'd never see independently. The GP's incentives are aligned through carried interest.

The friction: Management fees of 1.5-2% annually on committed (not just invested) capital. Performance fees of 20% on gains above a hurdle. You're writing a blank check to a blind pool. You can't choose which companies the fund buys. Lockups run 7-10+ years with almost zero liquidity.

Ticket sizes: Institutional-quality funds typically require $1-10 million minimums. Some emerging managers accept $250K-500K. Feeder funds and platforms can pool capital to meet higher minimums, but add another fee layer.

This path works if you want true diversification across deals and managers, you're comfortable delegating entirely, and you have enough capital to build a portfolio across vintage years. It's buying exposure to the asset class, not to specific opportunities.

Co-Investments

Think of these as sidecar deals. A fund manager invites you to invest directly alongside them in a specific transaction, usually with reduced or zero management fees and lower carry.

Why do GPs offer these? They need additional equity to close larger transactions. They're also cultivating relationships with LPs who might commit to future funds.

What works: Dramatically lower costs. Clear visibility into exactly what you're buying. You can cherry-pick deals rather than accepting everything in a blind pool. The GP has already done the heavy lifting on sourcing and due diligence.

The friction: Time-sensitive decisions (you might have days, not weeks). You're relying on someone else's underwriting. You need existing relationships to even get the call. And there's selection bias — GPs tend to offer co-investment in their highest-conviction deals, but it's worth asking why they need additional capital.

Ticket sizes: Typically $500K-$5M, though some opportunities go lower.

Co-investing is the practical middle ground for investors who want more control without building their own sourcing operation. But it requires a network, not just capital.

Direct Investments

This is the DIY version. You source companies independently. No fund structure. No GP taking carry. You negotiate terms, structure deals, and own everything directly.

What works: Complete control. Customised deal structures. You keep 100% of the upside minus transaction costs. You can apply your specific expertise or industry knowledge.

The friction: Sourcing quality deal flow is genuinely hard. Risk concentration is real since you're not diversified across 20 portfolio companies. You need your own team (legal, financial, operational) to execute properly. Post-investment, you may need to be actively involved in governance.

Ticket sizes: Direct minority growth investments can work at $2-5M. Meaningful control positions typically require $10M or more. Lead positions in buyouts often start north of $25M.

If you choose this path, you're building an investment operation, not just making investments. For founders considering this alongside an acquisition strategy, the skill sets overlap significantly.

Selecting Fund Managers: The Skill That Matters Most

Remember that 14-18% return dispersion between top-quartile and bottom-quartile funds? That's not noise. It's the entire game.

Fifth Third Private Bank's research puts it starkly: over a full market cycle, public large-cap equity funds show a performance differential of maybe 200 basis points between the top and bottom. Private equity funds show 1,000–1,500 basis points. Manager selection isn't important in PE. It's everything.

What actually separates great GPs from the rest:

Track Record Analysis (Done Right)

Past performance isn't just about IRR numbers. You need to understand how they got there.

First, look at consistency across market cycles. A manager who delivered 25% IRR during a bull market tells you less than one who generated solid returns through a downturn. CAIS research shows that 70% of funds following a first-quartile performer end up above the median. Performance does persist, but only when you're comparing apples to apples across vintages.

Second, examine the sources of the returns. Did they build value operationally? Or did they simply ride multiple expansions during easy money? One fund might have doubled EBITDA through genuine improvements. Another might have bought at 8x and sold at 12x without touching the business. Same return, completely different skill set.

Third, watch for unrealised investments. When GPs are fundraising for a new fund, a significant portion of their previous fund often remains unrealised. These unrealised companies can mask deteriorating performance. Ask what percentage of reported returns comes from realised exits versus mark-to-market valuations on holdings.

Reference Checks That Matter

Talk to people who've actually worked with the GP. Not the references they provide. Those are curated. Find former portfolio company executives. Talk to co-investors from previous deals. Reach out to other LPs in their funds.

The questions that reveal the most: How does the GP behave when things go wrong? Do they add value beyond capital, or are they financial engineers? What's their relationship with management teams like? Have you ever seen them act against their own short-term interest to do the right thing?

Team Stability

Private equity is a people business. If the partner who generated the track record has left, you're betting on a different team than the one that created the returns.

Look at turnover at all levels. Senior departures are obvious red flags. But watch mid-level turnover too. If associates and VPs keep leaving, something's broken in the culture. The best firms retain talent because they share economics fairly and invest in development.

Strategy Consistency

Be cautious when a GP pivots into new sectors or deal sizes. A lower-middle-market industrials specialist doesn't automatically know how to invest in enterprise software. Growth can dilute the edge that generated past success.

The CFA Institute framework emphasises that investment philosophy should be clear and consistent. Can the GP articulate exactly what market inefficiency they exploit and why they're uniquely positioned to capture it? If the answer is vague or changes with market trends, be careful.

Fee Alignment

The best GPs make most of their money from carried interest, not management fees. When management fees account for a disproportionate share of compensation, incentives shift toward raising larger funds rather than generating returns.

Ask how carried interest is distributed. Is it concentrated among founders, or spread across the team executing deals? GP commitment matters too. When principals have meaningful personal capital alongside yours, their interests align with yours.

Which brings us to the phenomenon reshaping how serious capital actually gets deployed.

Everything here is free. Subscribing just tells me the content is useful — and helps me decide what to write next.

Club Deals: The Quiet Revolution

Club investing is where multiple high-net-worth investors or family offices pool capital into a single transaction. No fund overhead. No blind pool. Just collective buying power.

According to PwC's Global Family Office Deals Study 2024, approximately 60% of family office PE transactions are now structured as club deals. This isn't a trend. It's becoming the default approach.

Why does this work?

Scale without concentration. You can participate in $50 million opportunities without writing the entire check. A group of five families can each put in $10M and access deals that would otherwise be impossible or imprudent on a standalone basis.

Expertise multiplies. Each participant brings different capabilities. One family might have deep operating experience in manufacturing. Another might have legal expertise in cross-border structuring. A third might have relationships in a specific industry vertical. Together, they create capabilities none possess individually.

Transparency and alignment. You know exactly who you're investing with and what you're buying. Terms are negotiated openly. There are no surprises about fee structures or conflicts.

Real-world examples show how this plays out. Pritzker Private Capital teamed up with Concentric Equity Partners and Duchossois Capital Management to recapitalize Energy Distribution Partners, a propane and light fuels distributor. Three Chicago-based family investment firms, each bringing different relationships and expertise, collaborated on a deal that worked better together than any could have executed alone.

At larger scale, look at the €17 billion acquisition of Thyssenkrupp's elevators business in 2020. Advent International and Cinven joined forces with the German foundation RAG-Stiftung and a major Middle Eastern sovereign wealth fund. Or the $34 billion Medline acquisition, where Blackstone, Carlyle, and Hellman & Friedman partnered with the same sovereign wealth fund. These consortium structures are now standard for deals above a certain size.

The practical challenge is finding the right partners. One family office executive described the core question well: it's less about finding people with capital, and more about finding people you'd want to be in business with for the long haul. The relationship matters as much as the capital.

Geographic Diversification: US, Europe, and Asia

Where you invest matters as much as what you invest in. Most family offices default to domestic opportunities because they're familiar. That leaves money on the table.

US: Scale, Depth, and Competition

The US remains the largest and most liquid PE market. According to McKinsey's 2025 Global Private Markets Report, US transaction volumes rebounded strongly in 2024-2025, with deals over $1 billion up 35% year-over-year.

The advantages are obvious. Deep capital markets. Mature secondary markets if you need liquidity. Robust legal frameworks. A massive universe of middle-market companies ripe for operational improvement.

The downside? Everyone knows this. Competition for quality deals is intense. Entry multiples for US buyouts remain elevated relative to historical averages. The abundance of dry powder (approximately $2.5 trillion globally as of mid-2025) means sellers have leverage.

Europe: Stable Premium, Different Dynamics

Bain & Company's analysis reveals something interesting: PE's outperformance versus public markets has been more stable and consistent in Europe than in the US. Part of this reflects Europe's more diversified public indices. Part of it reflects less competition for deals.

Europe offers exposure to different economic cycles and regulatory environments. The UK, Germany, and Nordic markets have mature PE ecosystems. Southern Europe and parts of Central Europe remain underpenetrated, with opportunities in family business successions.

Currency is a consideration. Euro and sterling exposure can provide natural diversification against dollar weakness. Some investors explicitly seek non-US assets as part of their jurisdictional strategy.

European GPs raised their highest levels of capital since 2007 in early 2025, benefiting from both moderation of US allocations and capital flowing from Asia.

Asia-Pacific: Complexity and Opportunity

Asia is where the picture gets nuanced. According to Bain's Asia-Pacific PE Report 2025, deal value increased 11% in 2024 after two years of decline. But that regional number masks dramatic divergence.

India was the standout performer. Double-digit growth in both deal value and count. A healthy IPO market providing real exit options. Growing domestic consumption. India became the region's largest exit market in 2024, surpassing Greater China for the first time.

Japan continues to attract capital as GPs seek stability, and corporate governance reforms are driving deal flow from corporate carve-outs and spin-offs.

China is the difficult question. As recently as 2020, China accounted for over half of the Asia-Pacific deal value. By 2024, that share fell to 27%. Geopolitical tensions, regulatory uncertainty, and economic headwinds have made Western investors cautious. Some GPs are exploring "China ex-China" strategies: companies headquartered elsewhere that benefit from Chinese demand without the direct exposure.

Southeast Asia offers growth characteristics but smaller deal sizes and less developed exit markets. Temasek's $10 billion private credit entity, launched in late 2024, signals growing institutional infrastructure.

The return dispersion in Asia is widening. Bain's data shows that top-quartile funds from the 2017 vintage delivered IRRs above 25%, while bottom-quartile funds barely reached the high single digits. More than ever, manager selection determines outcomes.

Practical Framework

For most family offices, a sensible geographic allocation might start with 60-70% domestic (where informational advantages and operational familiarity run deepest), 20-30% in developed markets like Europe, Japan, and Australia for diversification, and 0-10% in emerging markets only with specific expertise or trusted GP relationships.

Don't chase geography for its own sake. Invest where you can add value or where you have genuine conviction in the manager. The worst outcome is being a passive LP in an unfamiliar market, unable to evaluate what's actually happening.

Due Diligence: What Actually Matters

Once you're in the deal flow, how do you separate genuine opportunities from disasters?

Research suggests 70-90% of M&A transactions fail to meet their intended objectives. The examples are instructive. HP's 2011 acquisition of Autonomy led to an $8.8 billion write-down after discovering accounting irregularities that somehow weren't caught in due diligence. During Verizon's acquisition of Yahoo, its investigation uncovered massive data breaches affecting all 3 billion Yahoo email accounts. The discovery reduced the purchase price by $350 million. Verizon at least caught it. Marriott acquired Starwood without discovering a reservation system breach that exposed passport numbers for millions of customers, costing them significantly in remediation.

The pattern is consistent: problems that seem obvious in hindsight were somehow invisible during the process.

Rigorous due diligence examines several dimensions:

Revenue Quality

Is the revenue recurring, or one-time? What's the trend in gross margins over the past three years? Can the company raise prices without losing customers? How sticky is the customer base — meaning what's the switching cost for a customer to leave?

For SaaS businesses specifically, watch monthly customer churn. High churn even if counterbalanced by new acquisition suggests the product isn't delivering value or the market is too competitive.

Customer Concentration

If more than 20% of revenue comes from a single customer, you have a risk worth understanding. It's not automatically a deal-breaker, but it changes the nature of what you're buying.

EBITDA Adjustments

Sellers love add-backs. "One-time" expenses that somehow occur every year. Non-recurring items that recur. Proforma adjustments for expenses that haven't actually been eliminated. WeWork's "community-adjusted EBITDA" became famous for creative accounting. Every company has its version. Look at the actual cash flow, not the presentation deck.

Working Capital

Cash conversion matters more than headline earnings. Understand seasonality. Look for unexpected liabilities. Ask whether the working capital in the deal reflects normalised levels or has been artificially reduced.

Cap Table and Structure

Is ownership clean? Are there legacy claims, shadow equity arrangements, or unclear rights? A messy cap table creates governance problems that compound over time.

Legal and Compliance

Pending litigation. Unresolved regulatory issues. Environmental liabilities. Employment disputes. IP ownership questions. Each can create post-close problems that consume management attention and capital.

The Team You Need

Never attempt serious due diligence alone. At minimum, you need a seasoned M&A lawyer familiar with the deal type, a quality-of-earnings accountant who specialises in private company diligence, a tax planning specialist to structure the transaction, and an industry expert who is not being paid by the seller.

Private deals don't have the disclosure protections of public markets. Nobody's making sure the numbers are clean except you. The risk is on you. So is the responsibility.

Exit Strategy: Understanding How You'll Get Paid

Something that seems obvious but gets overlooked constantly: you make money in private equity when you exit. Not before. No matter how good the entry price or how well the company performs, unrealized returns are just accounting entries until you actually sell.

The exit environment has changed dramatically. According to McKinsey research, average buyout holding periods have stretched to 6.7 years, up from a two-decade average of 5.7 years. The exit backlog is larger than at any point since 2005.

Understanding exit paths isn't just about patience. It's about evaluating deals properly from the start.

The Main Exit Routes

Strategic Sale to a Corporate Buyer remains the gold standard. In 2024, strategic sales accounted for 55% of US PE exit value. A strategic buyer often pays a premium because they can extract synergies you can't. They might integrate the company into existing operations, expand distribution, or eliminate redundant costs.

During due diligence, map the logical acquirers. Who would benefit most from owning this business? Are they active acquirers? Have they bought similar companies before? If you can't identify at least three plausible strategic buyers, you're taking more exit risk than you might realise.

A Secondary Buyout (Sponsor-to-Sponsor) occurs when another PE firm acquires the company. This has become increasingly common. PitchBook data shows that secondary buyouts accounted for 30.5% of PE exits in early 2024, up from 25.2% the prior year.

Secondary exits can be faster and more certain than strategic sales. The buyer knows how to underwrite PE-backed businesses. But they're also buying with their own return expectations, which limits how much they're willing to pay. There's a school of thought that asks: if this is such a great business, why couldn't the first sponsor grow it further? That scepticism can pressure valuations.

IPO is often discussed but rarely achieved. IPOs made up just 5% of global PE exits in 2024. The bar is high. You need substantial scale, clean financials, a compelling growth story, and favourable market conditions. Post-IPO performance of PE-backed companies has been mixed in Europe, making underwriters selective.

IPOs also don't provide immediate liquidity. Lock-up periods typically prevent sponsors from selling for 180 days. And you're subject to market volatility throughout.

Continuation Funds have emerged as a significant fourth option. According to CFA Institute analysis, continuation vehicles accounted for 14% of all PE exits in 2024, up from 12.9% the prior year. Analysts expect this could reach 20% in coming years.

In a continuation fund, the GP transfers assets from an old fund to a new vehicle. Existing LPs can cash out or roll their investment. It's a way to extend holding periods without forcing a sale at suboptimal timing. But it creates potential conflicts since the GP is on both sides of the transaction. Insist on independent valuations and understand the governance structure before rolling over.

Recapitalization involves restructuring the company's debt and equity, often returning capital to investors while maintaining ownership. Dividend recaps have become popular in the current environment, letting GPs make distributions without full exits. This preserves upside but can also signal that full exit options are limited.

Evaluating Exit Potential During Diligence

When analysing any deal, explicitly assess:

- Size and trajectory: Is the company growing toward a scale that attracts strategic acquirers? Most corporate buyers want acquisitions above a certain threshold to justify integration costs.

- Market structure: Are there active consolidators in this industry? Has M&A activity been robust? Or is this a fragmented market where exits typically go to financial sponsors?

- Timing considerations: What's the realistic path to exit-ready? If significant operational work remains, factor in longer holding periods.

- Current owner motivations: Why is the seller exiting now? If they're choosing to sell after a long hold, it may signal limited further upside.

The sponsors handling the current environment successfully aren't waiting for conditions to improve. They're underwriting realistic exit scenarios from day one and structuring deals that don't depend on perfect timing.

Case Studies: A Success and a Failure

Theory only takes you so far.

Success: Blackstone's Hilton Hotels

In 2007, Blackstone acquired Hilton Hotels for $26 billion in one of the largest leveraged buyouts in history. The timing looked terrible. They closed the deal just before the global financial crisis, which devastated the hospitality industry.

What went right:

Blackstone recognized that Hilton's problems were operational, not structural. The brand was strong. The real estate footprint was valuable. But the company had underinvested in properties and international expansion.

Rather than panic selling during the crisis, Blackstone extended holding periods and focused on fundamental improvements. They renovated properties. They expanded internationally, particularly in high-growth markets. They invested in the loyalty program. They negotiated better terms with property owners who needed capital during the downturn.

By 2013, Hilton was ready for the public markets. The IPO raised $2.35 billion, the largest hotel IPO ever. Blackstone eventually realized returns estimated at nearly $14 billion on its equity investment, roughly tripling its money despite buying at what looked like the worst possible moment.

The lesson: Entry timing matters less than business quality and operational execution. A great asset bought at a tough time can still generate exceptional returns if you have the conviction (and capital) to hold through volatility and add genuine value.

Failure: Toys "R" Us

In 2005, KKR, Bain Capital, and Vornado Realty Trust acquired Toys "R" Us for $6.6 billion. It became one of the most studied examples of PE failure.

What went wrong:

The acquisition loaded the company with approximately $5 billion in debt. Annual interest payments exceeded $400 million. This debt service consumed cash that could have funded store renovations and e-commerce investments.

Meanwhile, the retail landscape was shifting dramatically. Amazon was expanding. Walmart was undercutting on price. Target was improving its toy selection. Toys "R" Us needed to transform. Instead, it was focused on servicing debt.

The company couldn't invest in its stores, which became dated and unappealing. It couldn't build competitive online capabilities. It couldn't match competitors on price because its cost structure was burdened by interest payments.

By 2017, Toys "R" Us filed for bankruptcy. By 2018, it liquidated entirely. Tens of thousands of employees lost their jobs. Creditors received cents on the dollar. The PE sponsors lost their equity.

The lesson: Leverage amplifies everything. In a stable industry, debt-funded buyouts can generate excellent returns. In an industry facing structural disruption, the same leverage can prevent necessary adaptation. The sponsors underestimated how quickly retail was changing and structured a deal that left no room for transformation.

The critical due diligence failure wasn't financial. It was strategic. They didn't adequately stress-test what would happen if the retail environment shifted dramatically. The model worked only if the business continued operating as it always had.

The Pattern That Emerges

Successful deals share common elements: buying quality assets with strong underlying positions, adding genuine operational value, and maintaining flexibility to hold through volatility.

The failures typically involve some combination of overpayment, excessive leverage, and inability to adapt to changing conditions. The PE sponsors weren't stupid. They were optimistic in ways that proved expensive.

When evaluating any deal, ask honestly: what's the realistic downside scenario, and can the capital structure survive it?

Private Credit: The Complement Worth Understanding

Private credit isn't the same as private equity, but the two increasingly work together in sophisticated portfolios. If you're allocating to PE, understanding how credit fits alongside equity exposure matters.

According to the Goldman Sachs 2025 Family Office Report, family office allocations to private credit rose to 4% in 2025, up from 3% in 2023. The proportion of family offices with zero private credit exposure dropped from 36% to 26%.

Why the interest? Senior direct lending typically offers spreads of 500-650 basis points over base rates with contractual cash flows. You're senior in the capital structure — paid before equity holders if things go wrong. Duration runs 3-5 years rather than PE's 7-10, meaning capital returns faster.

But this asset class is being stress-tested right now. In early 2026, Blue Owl halted redemptions and AI began dismantling business models underlying a quarter of the private credit market. The assumptions behind many founders' private credit allocations are under pressure simultaneously.

That doesn't make the asset class uninvestable. It means the same rigorous manager selection that matters in PE matters equally in credit. For a deeper look at how to evaluate this space with clear eyes, see the full Private Credit Playbook.

Building Deal Flow: Network as Investment Edge

All of this presumes you can actually access deals. Which brings us to the practical question most people avoid: how do you build the relationships that generate real opportunities?

The Reality of Access

Quality deal flow is a function of reputation and relationships, not capital alone. There's more money chasing private deals than ever. What distinguishes investors who see the best opportunities from those who don't?

The families and offices with consistent access have built something over years. They're known quantities. GPs, investment bankers, and founders know what they invest in, how they make decisions, and whether they're reliable partners.

If you're starting from scratch, that's a multi-year project. There are no shortcuts. But there are strategies that work.

Where Deals Actually Come From

Existing GP relationships: If you're already investing in funds, those relationships are your first source of co-investment and direct deal flow. Make yourself useful. Provide value beyond capital. GPs share opportunities with LPs they trust and enjoy working with.

Investment banks and intermediaries: Lower-middle-market investment banks often have mandates too small for institutional PE but perfect for family offices. Build relationships with 2-3 bankers who cover industries you understand. They're incentivised to bring you into processes if you can close.

Independent sponsors: These are PE professionals without committed funds who source deals and then find capital for specific transactions. They need investors like you. The M&A Source tracks this as a growing channel for family office deal flow.

Operating advisors and executives: Former CEOs and operators often see opportunities before they reach formal processes. Board members get approached about deals. Building a network of operating executives in your target sectors can generate proprietary deal flow.

Family office networks: Peer families are often the best source of club deal opportunities. Groups like the Institute for Private Investors and Family Office Club facilitate these connections through conferences and ongoing platforms. The value isn't just deal sharing. It's learning from peers who've made similar investments and can share reference points.

Industry conferences: The right events put you in proximity with entrepreneurs, sellers, and intermediaries. This isn't about attending generalist investor conferences. It's about going deep in specific sectors where you want to build a reputation.

Building Your Reputation

Access ultimately flows from reputation. How do you build one?

Develop genuine expertise. The most effective family office investors have clear focus areas where they've accumulated real knowledge. Maybe it's healthcare services. Maybe it's industrial distribution. Maybe it's software businesses serving specific verticals. Depth beats breadth for generating proprietary flow.

Be reliable and fast. When you see a deal, respond quickly with clear feedback. Either you're interested and moving forward, or you're not. Nothing damages reputation faster than wasting people's time on deals you were never serious about.

Add value beyond capital. Can you make introductions? Share operational experience? Provide references? The investors who get the best access are genuinely helpful to the entrepreneurs and sponsors they work with.

Close deals. All the relationship-building in the world matters less than actually getting transactions done. A track record of closed deals opens doors that networking alone cannot.

The practical reality: start with one or two sectors where you have genuine interest or expertise. Build relationships systematically in those areas. Be patient. Quality deal flow is a lagging indicator of reputation built over years, not months.

Practical Capital Requirements

A realistic framework for what it takes:

| Strategy | Typical Investment Size |

|---|---|

| Fund Investment (feeder/platform) | $100K - $500K |

| Fund Investment (direct LP) | $1M - $10M |

| Co-Investment | $500K - $5M |

| Direct Minority Deal | $2M - $20M |

| Buyout (Lead Investor) | $10M - $100M+ |

Exceptions exist in every category, but this gives the framework.

Time horizons matter. Private equity is long-term by design. Capital typically gets locked up for 7-12 years. Distributions happen when the GP decides, not when you need liquidity. That means maintaining a buffer elsewhere — this isn't capital you can afford to need back on your timeline.

Building a Portfolio That Makes Sense

A sensible private markets allocation might look like 50% in traditional funds (for diversification and access to institutional-quality managers), 30% in co-investments (for cost control and selectivity), and 20% in direct or club deals (for high-conviction, custom opportunities).

Ladder investments across multiple vintage years. Diversify across sectors. Avoid concentrating in one strategy or one manager. For founders thinking through how this fits within broader portfolio construction, PE is one component of a wider allocation framework.

BNY Mellon's 2025 research found that 64% of family offices anticipate making six or more direct investments in the coming year, a 10% increase from the previous twelve months. They're not abandoning fund investing. They're blending approaches based on opportunity.

Think like an institution. But stay nimble enough to move when quality deals surface.

Access Beats Alpha

The challenge in private equity isn't finding alpha. It's accessing it.

Your edge as a private investor doesn't come from outguessing markets or picking the perfect entry multiple. It comes from building relationships, sourcing better deals, and structuring investments intelligently.

As direct and club deals become standard for sophisticated capital, the game is shifting. Passive capital doesn't get invited back. Engaged, value-adding capital partners do.

That means building your network deliberately rather than opportunistically, developing genuine expertise in sectors you understand, creating repeatable diligence processes you can execute consistently, and learning deal structuring beyond basic terms.

The families and offices doing this well aren't just writing checks. They're building capabilities. They're developing reputations as good partners who add value beyond capital.

Because in private equity, who you know determines what you can access.

And access is everything.

Capital Founders OS is an educational platform for founders with $5M–$100M in assets. Frameworks for thinking about wealth — so you can make better decisions.

Explore more: Playbooks · Capital Signals · Wealth Architecture · Investment Strategy · Business Building · Life Design

Found this useful? Forward it to a founder who's thinking about this stuff. Got a question or disagree with something? Get in touch.

New here? Subscribe for one email a week.