There's a particular kind of founder who reads every financial headline, tracks their portfolio daily, and still refuses to borrow a dollar against it.

They'll negotiate a $30 million exit, diversify into index funds, buy real estate outright — and leave millions in potential value on the table because the word "debt" triggers something deep and reflexive. Strategic leverage never enters the conversation.

That reflexive aversion made sense during the building years. Bootstrapping teaches you that debt is dangerous, cash is oxygen, and owing people money means losing control. Those lessons build companies. They also create a blind spot that costs serious money once you're managing personal wealth.

Wealthy families — the ones compounding capital across two or three generations — think about debt completely differently. For them, borrowing isn't a sign of weakness. It's infrastructure. It sits alongside tax planning, estate structures, and portfolio construction as one of the fundamental tools of wealth architecture.

The gap between how first-generation founders use debt (barely) and how established wealth uses it (strategically) is one of the largest inefficiencies in the $5M–$100M wealth bracket.

Closing that gap starts with understanding how the mechanics actually work.

What This Post Covers

- Loan proceeds aren't taxable income: Borrowing against appreciated assets avoids capital gains while the portfolio keeps compounding. A US founder needing $2M in liquidity can save $515,000+ by borrowing instead of selling

- Securities-based lending is a $138B market: Morgan Stanley's wealth management lending doubled from $71.5B to $147B between 2019 and 2024. The infrastructure exists — most founders in the $5M–$50M range don't use it

- Buy, borrow, die is real strategy: Hold appreciating assets (no tax), borrow when cash is needed (no taxable event), pass to heirs with stepped-up basis. The Joint Committee on Taxation estimates this costs $58B in forgone federal revenue annually

- Concentration plus leverage kills: Bill Hwang turned $10–15 billion into an 18-year prison sentence through 5:1 leverage on concentrated positions. Every leverage catastrophe shares the same ingredients: concentration, excessive leverage, insufficient reserves

- Conservative sizing beats clever strategy: Overall portfolio leverage below 25–30% of liquid net worth, 12–18 months of interest in cash reserves, and never leveraging a concentrated position beyond 20% LTV

Why Founders Have an Emotional Block Against Debt

Bootstrapping selects for a specific relationship with borrowed money. Every founder who built a company without outside capital treated debt as a threat to survival. And they were right — early-stage business debt with personal guarantees and uncertain cash flows genuinely is dangerous.

The problem is that this hard-won instinct doesn't automatically recalibrate after a liquidity event.

A founder sitting on $20 million in diversified assets has an entirely different risk profile than one running a company on a $50,000 credit line. But the emotional circuitry doesn't update that fast. The body remembers what the balance sheet has forgotten.

Even founders who raised equity during the building phase often carry residual aversion. They understand dilution and cap tables instinctively, but personal leverage feels different — more exposed, more like betting against yourself.

There's also the cultural messaging. Personal finance media overwhelmingly target people for whom debt really is dangerous. "Debt is bad" is solid advice for someone earning $80,000 a year with no assets. It's actively misleading for someone with $15 million in liquid securities generating 8% annually.

The shift from Growth Mode into Owner Mode demands rethinking everything. Including your relationship with borrowed money. Operators eliminate debt. Owners and allocators deploy it.

Good Debt Versus Destructive Debt

Not all borrowing is created equal.

Destructive debt has a few hallmarks: it finances consumption that depreciates, carries high interest rates, is unsecured or poorly structured, and comes with terms that blow up under stress. Credit card balances, unsecured personal loans for lifestyle purchases, and margin accounts funding speculative positions all live here.

Strategic debt looks different:

- It's asset-backed — something valuable sitting behind it

- It's tax-efficient — generating deductible interest or avoiding taxable events

- It's appropriately sized — with substantial headroom before stress scenarios trigger trouble

- Its terms align with the borrower's actual situation

- The cost of borrowing sits below the expected return on the assets it's freeing up

The simplest example is a mortgage on a primary residence. A founder worth $25 million who pays cash for a $4 million home feels prudent. A founder who puts 30% down and takes a mortgage at 5.5% while keeping $2.8 million invested at a long-term expected return of 8–10% is making a rational capital allocation decision. The maths favours leverage, even accounting for interest cost, because the invested capital compounds over decades while the loan's real cost erodes with inflation.

Multiply that logic across a full balance sheet — real estate, securities, operating businesses — and the compounding advantage becomes substantial. Lombard lending dates to 14th-century Italian merchant families. The mechanics haven't changed because the maths hasn't changed.

Securities-Based Lending: How It Works

Securities-based lending (SBL) is probably the single most underused financial tool for founders with liquid portfolios. The concept is simple: borrow against the value of your investment portfolio without selling anything. Your stocks, bonds, and funds serve as collateral. You get cash. The portfolio stays invested.

In the US, these are typically called securities-based lines of credit (SBLOCs). In European private banking, the equivalent product is a Lombard loan — more on that shortly.

Basic Mechanics

A diversified portfolio of publicly traded securities typically supports a loan-to-value (LTV) ratio of 50–70%, depending on concentration and volatility. Government bonds can push LTV as high as 90%. Single-stock positions or volatile holdings might drop below 30%.

You draw funds as needed, pay interest only (usually pegged to a reference rate like SOFR plus a spread), and repay principal at maturity or whenever you choose. The portfolio remains fully invested throughout, continuing to generate returns, dividends, and compounding growth.

Setup is usually fast — often days rather than weeks — because underwriting focuses on portfolio quality rather than personal income documentation. Goldman Sachs advertises its securities-based loans with "no personal financial statements, tax returns, or paper applications."

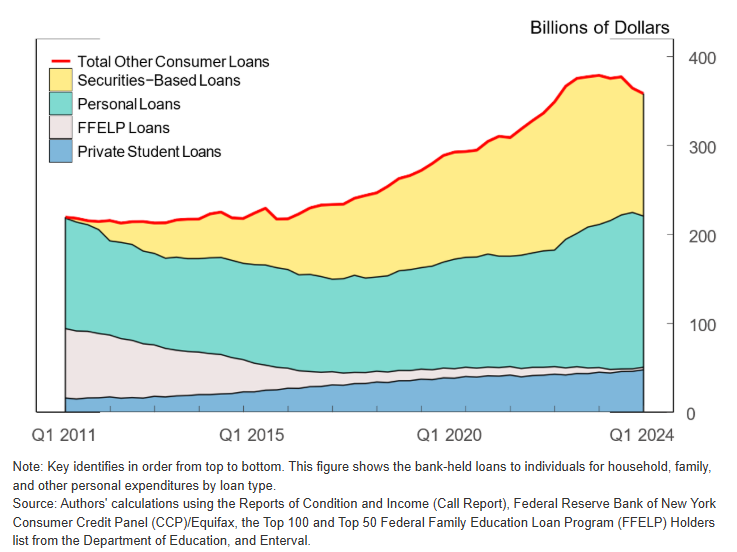

Scale of the Market

This isn't niche. The Federal Reserve estimated that as of Q1 2024, securities-based loans outstanding in the US totalled approximately $138 billion. Combined with roughly $180 billion in margin loans, the total asset-based consumer lending sector sits at approximately $318 billion.

The growth trajectory tells the story of adoption. Morgan Stanley's wealth management lending more than doubled from $71.5 billion in 2019 to over $147 billion by Q1 2024. Goldman Sachs plans to double its lending to clients worth $10 million or more within five years. Bank of America and JPMorgan both carry wealth management loan books exceeding $200 billion each.

The infrastructure exists. Most founders in the $5M–$50M bracket simply don't know about it.

How SBLs Create Tax Efficiency

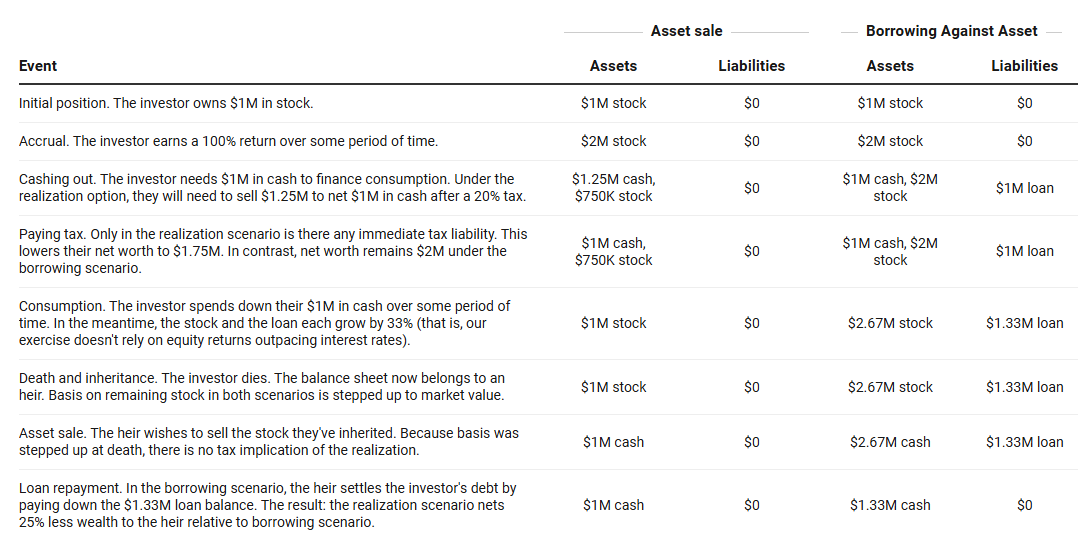

The core tax advantage: loan proceeds are not taxable income. Unlike selling securities — which triggers capital gains tax — borrowing against them creates zero tax liability. The portfolio keeps compounding without interruption.

Here's how the maths plays out in practice. A US founder in a high-tax state holds $10 million in equities with a $3 million cost basis ($7 million in unrealised gains). They need $2 million in liquidity.

If they sell: Roughly $1.4 million of the $2 million sold represents a gain. Federal capital gains at 23.8% (including the 3.8% net investment income tax) create a bill of approximately $333,000. In California, add another $182,000 in state tax. Total tax hit: roughly $515,000. Gone permanently. And the lost compounding on $515,000 over 20 years at 8% exceeds $2.4 million.

If they borrow: A $2 million SBLOC at 5.5% interest costs $110,000 per year. The full $10 million stays invested. Over five years, total interest: $550,000. But the portfolio has been compounding on $10 million instead of $8 million. The net benefit of borrowing widens with every passing year.

The second tax advantage is subtler but important: interest payments may be deductible. Under US tax law, investment interest expense can be deducted against investment income. If your portfolio generates dividends and interest income, the borrowing cost can offset that income dollar-for-dollar, further reducing the net cost.

Third — and this matters for founders who still hold concentrated positions — borrowing avoids having to reset your basis. Selling shares triggers a permanent taxable event. Borrowing preserves the ability to donate those shares to charity at full market value later, transfer them to trusts, or pass them to heirs with a stepped-up basis. The tax optionality preserved by not selling is itself valuable.

ProPublica's landmark investigation into IRS data revealed that the 25 richest Americans paid an average true tax rate of just 3.4% between 2014 and 2018. The mechanism is exactly this: hold appreciating assets, borrow against them rather than sell, and never trigger a capital gains event. As of 2022, Elon Musk had pledged $94 billion in Tesla shares as collateral for personal loans.

The mechanics work the same way at $5 million, $20 million, or $100 million. The tax savings scale proportionally. The only thing that changes at lower asset levels is access — and that access has widened considerably in the past five years.

Lombard Loans: The International Private Banking Version

Outside the US, the same concept is known as a Lombard loan. Named after medieval Lombard merchants who pioneered lending against moveable collateral, it's been a cornerstone of European private banking for generations.

How Lombard Loans Differ From US SBLOCs

The mechanics are similar, but the product is structured to offer greater flexibility for internationally mobile clients.

Typical LTV ratios by collateral type:

- Investment-grade government bonds: 70–90%

- Diversified blue-chip equity portfolios: 50–70%

- Single-stock positions in major indices: 30–50%

- Concentrated or volatile positions: 20–30%

- Private equity and hedge fund holdings: rarely accepted

Swiss private banks pioneered the modern Lombard facility and tend to apply conservative haircuts by asset class. A blue-chip equity position might have an LTV of 60–70%, while a speculative holding could be capped at 30%. A Deloitte global survey of 150+ financial institutions found that even crypto-backed Lombard loans are emerging, with typical Bitcoin LTV ratios of 25–40%.

The key advantage is flexibility. Proceeds can fund almost any purpose: property purchases, business investments, bridge financing, or tax payments. Repayment is often interest-only with principal due at maturity or rolled into a new facility.

Tax Optimisation Through Lombard Lending

Lombard loans mirror SBLOCs in their core tax mechanics but add cross-border advantages that matter for globally mobile founders.

Avoiding capital gains across jurisdictions. A UK-resident founder holding a portfolio managed in Switzerland can borrow through a Lombard facility to purchase property in Portugal — accessing liquidity without triggering UK capital gains tax, Swiss withholding implications, or Portuguese property-related selling costs. The assets stay invested in their original jurisdiction. No taxable event in any country.

Currency flexibility. Unlike most US products, Lombard facilities often allow borrowing in multiple currencies against a single portfolio. A founder with USD-denominated assets can borrow in GBP for a London property or EUR for continental expenses, without the tax and transaction costs of currency conversion through asset sales.

Interest deductibility varies by jurisdiction. In some locations, interest on Lombard facilities may be deductible against investment or business income, depending on how proceeds are deployed. The specifics require local tax advice, but the principle holds: borrowing costs may be partially subsidised by the tax system.

Preserving estate planning optionality. Like SBLOCs, Lombard loans avoid crystallising gains and preserve the ability to use those assets in family trusts, charitable structures, or intergenerational transfers at their current basis. For founders thinking about long-term wealth transfer, this flexibility can be worth significantly more than the interest cost.

Willow Private Finance describes a typical case: a client with a £5 million portfolio uses a 60% LTV Lombard facility to release £3 million for a London property, avoiding a large capital gains liability. The assets remain invested. Within 12 months, the client refinances with a conventional mortgage. This hybrid approach — immediate Lombard liquidity followed by long-term financing — is increasingly standard in prime property markets.

The "Buy, Borrow, Die" Strategy

There's a wealth strategy so effective and controversial that it has its own name.

Coined by Professor Edward McCaffery at USC in the 1990s, "buy, borrow, die" describes how wealthy families build, access, and transfer wealth while minimising tax at every stage.

Step 1: Buy. Acquire appreciating assets and hold them. Unrealised gains aren't taxable. A portfolio growing from $10 million to $50 million over 20 years creates zero capital gains tax as long as nothing is sold.

Step 2: Borrow. When cash is needed, borrow against the assets rather than sell. Loan proceeds aren't income. No tax event. The portfolio keeps compounding.

Step 3: Die. Under current US tax law, heirs receive a "stepped-up basis," resetting cost to fair market value at death. Decades of unrealised gains effectively disappear for income tax purposes.

The Joint Committee on Taxation estimates that stepped-up basis accounts for $58 billion in forgone federal revenue in 2024, rising to $68 billion by 2027. The Budget Lab at Yale published a detailed reform analysis in 2025, noting that while borrowing represents only about 1% of total income for the top 0.1%, the real driver is the ability to defer gains indefinitely.

For founders in the $5M–$100M range, the full playbook may not apply exactly as it does for billionaire dynasties. But the principles — hold appreciating assets, borrow rather than sell, structure transfers to minimise friction — absolutely scale down. This window may also not remain open indefinitely. Proposed reforms, including the ROBINHOOD Act and calls to eliminate stepped-up basis, are gaining political momentum.

Real Estate and Other Forms of Strategic Leverage

Real estate leverage remains the oldest and most widely understood form of strategic debt: use a small amount of equity to control a larger asset, let rental income or appreciation do the work, benefit from tax deductions on interest and the inflation-driven erosion of the loan's real value. The same logic extends to business acquisition financing, insurance premium financing for large life policies, and art lending against high-value collections.

The sizing question matters across all of these. Conservative leveraging means keeping total debt below 50% of asset values with income comfortably covering at least 1.25x debt service. Pushing leverage ratios to greater levels materially changes the risk profile — the difference between sleeping through a downturn and facing a liquidity crisis. For more on how real estate fits into a broader portfolio, see our dedicated playbook.

When Leverage Destroys Wealth

No honest discussion of debt can skip the catastrophic examples. And understanding what goes wrong matters as much as understanding the investment philosophy behind what goes right.

Bill Hwang and Archegos Capital Management provide the most instructive recent case. Before March 2021, Hwang's wealth was estimated at $10–15 billion, built through concentrated, leveraged positions in a handful of stocks using total return swaps. His leverage ratio: roughly 5:1, according to SEC filings and DOJ indictment documents.

When several positions declined simultaneously, margin calls cascaded. Within 48 hours, roughly $20 billion in personal wealth evaporated. Banks collectively lost over $10 billion. Credit Suisse's $5.5 billion hit contributed to the institution's eventual collapse and led to its merger with UBS in 2023. In July 2024, a federal jury convicted Hwang on 10 of 11 criminal counts, including securities fraud, racketeering, and market manipulation. He was sentenced to 18 years in prison and ordered to pay over $9 billion in restitution.

The Archegos collapse illustrates every leverage-related risk simultaneously: extreme concentration in a handful of correlated stocks, a leverage ratio where a 20% decline wipes out equity, positions hidden across six prime brokers with none seeing the full picture, and the margin call doom loop where forced selling drives prices lower and triggers more calls.

In 1998, Long-Term Capital Management repeated the same pattern at 25:1 leverage. The 1929 crash was fuelled by margin accounts requiring just 10% equity. The 2008 crisis was driven by leveraged mortgage-backed securities.

The common thread in every leverage catastrophe: concentration plus excessive leverage plus insufficient reserves.

Strategic Leverage: Guidelines and Red Lines

Five Questions Before Borrowing

- What specific problem does this borrowing solve? Liquidity access, tax efficiency, maintaining investment exposure, bridge financing? If the quantifiable benefit can't be articulated in one sentence, the case for borrowing is weak.

- What happens if collateral drops 30–40%? Meeting margin calls from cash reserves without forced selling is the baseline. If that's not possible, the position is too large.

- Am I combining leverage with concentration? Borrowing against a diversified portfolio is a liquidity tool. Borrowing against a single stock is a leveraged bet. The distinction matters more than most people realise.

- Do I have 12–18 months of interest payments in liquid reserves? This buffer is the difference between riding out volatility and becoming a forced seller.

- Have I coordinated with my tax advisor? The value of leverage strategies depends entirely on jurisdiction, cost basis, and estate planning goals.

Sizing Guidelines: LTV Ratios by Asset Type

| Asset Type | Typical LTV Range | Risk Level |

|---|---|---|

| Government bonds (investment grade) | 70–90% | Low |

| Diversified global equity portfolio | 50–70% | Low-Moderate |

| Blue-chip single stocks (large-cap) | 40–60% | Moderate |

| Mid/small-cap or volatile equities | 20–40% | Higher |

| Concentrated single-stock position | 20–35% | High |

| Hedge fund or PE holdings | 0–25% | Very High |

| Real estate (mortgage) | 60–80% | Varies by jurisdiction |

| Crypto (BTC/ETH) | 25–40% | Very High |

Overall portfolio leverage ceiling: Most conservative advisors recommend staying below 25–30% of liquid net worth. In the early post-exit years, 15–20% is a common starting point.

Red Lines — Non-Negotiable

- Never leverage a concentrated position beyond 20% LTV. If 80%+ of net worth sits in one stock and is borrowed against, a 25% decline triggers margin calls that force selling at the worst moment.

- Never use borrowed funds to buy more of the same asset class. Borrowing against equities to buy more equities doubles the directional bet. This creates doom loops.

- Never borrow without understanding margin call triggers. The exact threshold value, the notice period, and what happens if the call can't be met — all of this needs to be understood before the first draw.

- Never let total debt service exceed 30% of passive income. Leave margin for life to happen.

- Never rely on collateral appreciation to service the debt. If the only way to repay is for the portfolio to keep climbing, that's not a strategy. That's a hope.

Decision Tree: When Borrowing Tends to Make Sense

Do you hold appreciated assets with significant unrealised gains?

- Yes → In a high-tax jurisdiction? → Yes → SBL/Lombard structures offer the clearest tax advantage here.

- Yes → Zero capital gains tax jurisdiction? → Yes → Tax advantage disappears, but maintaining investment exposure may still justify borrowing at conservative LTV.

- No significant gains → Tax benefit is minimal. Conventional financing is likely more straightforward.

Is the purpose productive or consumptive?

- Property, business investment, bridge financing → These are the strongest candidates for leverage

- Lifestyle purchase, car, holiday → Most conservative advisors would flag this as consumption debt, not strategic leverage

Is your portfolio diversified?

- Yes, across asset classes and geographies → Borrowing against it is relatively low-risk at conservative LTV

- No, concentrated in a few positions → Very low LTV and caution warranted, or concentrated position strategies worth exploring first

Can you survive a 40% drawdown without forced selling?

- Yes → The drawdown risk is manageable at conservative LTV

- No → Building a larger cash buffer or reducing position size comes first

RED STOP — Warning signs that leverage is not appropriate:

- Total leverage would exceed 30% of liquid net worth

- Less than 12 months of interest payments held in cash reserves

- Collateral is a single concentrated position

- The borrowing is motivated by chasing returns or speculating

- There's pressure to deploy capital quickly

The founders who handle leverage well treat it like they treated every other major business decision — with specifics, not generalities. They know their LTV ratios by asset class, their margin call thresholds by facility, and their interest coverage in a stress scenario. They know what they won't do. And they figured out those limits before they needed the money, not while a margin call was ticking down.

Treasury management, borrowing capacity, and cash reserves all connect. Treating them as separate decisions is how quiet mistakes become expensive ones.

Capital Founders OS is an educational platform for founders with $5M–$100M in assets. Frameworks for thinking about wealth — so you can make better decisions.

Explore more: Playbooks · Capital Signals · Wealth Architecture · Investment Strategy · Business Building · Life Design

Found this useful? Forward it to a founder who's thinking about this stuff. Got a question or disagree with something? Get in touch.

New here? Subscribe for one email a week.